Sagebrush Sam's

Executive Summary

Sagebrush Sam’s – “a steak buffet,” unlike a typical restaurant, will provide a unique combination of excellent food at value pricing with a fun and entertaining atmosphere. Sagebrush Sam’s is the answer to an increasing demand. The public (1) wants value for everything that it purchases, (2) is not willing to accept anything that does not meet its expectations, and (3) wants entertainment with its dining experience.

In today’s highly competitive environment, it is becoming increasingly more difficult to differentiate one restaurant concept from another. Sagebrush Sam’s does this by being the only buffet concept that features mesquite-grilled, USDA-choice sirloin steaks, cooked on our display grill, for one low price. We will be serving top quality, 21-day aged steaks that are hand-cut daily on the premises and seasoned to perfection. Our grill will be out in the open and loaded with steaks cooked to the proper degree of doneness that our guests request. With our high dinner volume, there will be no waiting for a steak since we will have the grill stocked with every degree of doneness. No other national chain has tapped this market. With red meat (in particular, steaks) increasing in demand today, we believe that this feature will ensure our success.

This restaurant business plan is prepared to obtain financing for the initial launch of this concept. The financing is required to begin work on kitchen design, architectural plans, manuals and recipe books, site selection, equipment purchases, and to cover expenses in the first year of business. Additional financing will need to be secured for the two subsequent units anticipated in July, Year 2 and January, Year 3. Our positive cash flow will help to offset some of this burden.

The financing, in addition to the capital contributions from the owners, will allow Sagebrush Sam’s to successfully open and maintain operations through year one. The initial capital investment will allow Sagebrush Sam’s to provide its customers with a value driven, entertaining dining experience. A unique, mid-scale, innovative environment is required to provide the customers with an atmosphere that will induce middle America to bring family and friends to dine and socialize. Successful operation through year three will provide adequate cash flow to be self-sufficient in year four.

Objectives

Sagebrush Sam’s objectives for the first three years of operation include:

- Growing one unit per year for the first three years of operation.

- Keeping food cost under 35% of revenue.

- Keeping employee labor cost between 16-18% of revenue.

- Averaging sales in each location between 3-4 million dollars per year.

- Maintaining tight controls on costs and operations by hiring a managing partner/proprietor for each location and utilizing automated computer/Internet control.

Mission

Sagebrush Sam’s will strive to be the premier buffet restaurant in the local marketplace. We want our guests to have the total experience when visiting Sagebrush Sam’s. Not only will our guests receive a great meal, they will also be provided with a fun atmosphere. We will be doing unique things (such as serving all-you-can-eat USDA-choice sirloin steaks on a display mesquite grill) that will set us apart from the competition. We will want the dining experience to be as pleasing to the senses as it is to the palate.

Our main focus will be serving quality food at a great value. We will feature a large selection of freshly-prepared food, most in full view of our guests. We will feature 100 items daily that are full of flavor and zest at an unbelievable price!

Customer satisfaction is paramount. When approached by a customer with a request, our motto will be, “Yes is the answer; what is the question?” We will strive for broad appeal. We want to be the restaurant of choice for everyone: families and singles, young and old, male or female.

Employee welfare will be equally important to our success. All will be treated fairly with the utmost respect. We want our employees to feel a part of the success of Sagebrush Sam’s. Happy employees make happy guests.

We will combine menu variety, atmosphere, ambiance, and friendly staff to create a sense of “place” in order to reach our goal of over-all value in the dining/entertainment experience.

Keys to Success

The keys to the success of Sagebrush Sam’s are:

- The creation of a unique, innovative, entertaining, mid-scale atmosphere that will differentiate us from the competition.

- Execution of our primary goal to serve nothing but the highest quality food at unbelievably low prices in a clean, fun environment. We must deliver on this pledge 100% of the time, without exception.

- Controlling costs at all times, in all areas.

- Hiring the best people available, training, motivating and encouraging them, and thereby retaining the friendliest, most efficient staff possible.

Company Summary

- Entertaining surroundings — All stores will feature display cooking of our featured USDA-choice sirloin steaks cooked over a mesquite grill. Our guests will also be able to view our meat-cutting cooler where steaks are hand-cut daily and aged for 21 days to ensure that they are so very tender. The bakery, salad, and hot food stations will also be visible to our guests while they pick out their favorites from over 100 deliciously-prepared items daily. Our walls will be decorated with Western antiques by (confidential or proprietary information deleted).

- Quality food — Each Sagebrush Sam’s will serve nothing but fresh meats, crisp salads, delectable side dishes and scrumptious desserts, all served with old-fashioned, home-style care!

- 1/3 lb. Sam’s Specialty Beefburger lunch — A special treat will greet our weekday lunch guests from 11:00 a.m. till 2:30 p.m. We will be serving 1/3 lb. Sam’s Specialty Beefburgers off our display grill. The Sam’s Specialty Beefburgers will be ground fresh daily and seasoned with our custom blend of spices designed to enhance their taste. To complement our sandwiches, we will convert one of our hot bars to a cold “sandwich fixin’s” bar, with sliced tomatoes, onions, chopped lettuce, pickles, relish and everything necessary to complement our sandwiches.

- Variety, variety, variety — A different menu for every day of the week will feature…(confidential or proprietary information deleted)…to name a few of our special theme dinners. We will also change the menu items quarterly on these nights to spice things up.

- Open only for peak business periods — Buffet food does not keep well during slow time periods because all hot food must be held above 140 degrees Fahrenheit. Therefore, we will close our doors weekdays between 2:30 p.m.- 4:00 p.m. and at 8:30 p.m. nightly except on Friday and Saturday when we will close at 9:30 p.m.

- Breakfast buffet — Depending upon location, Sagebrush Sam’s will serve a buffet breakfast, offering fresh fruits in-season, cold juices, hot breakfast items, and cook-to-order omelets from our display grill. Some locations may offer breakfast daily while others may only feature it on weekends.

- Self-service — Every new guest will receive a guided tour explaining our concept and the self-serve system. We have found that by doing this we can exceed our guest perception of service 96.5% of the time. For example, if a guest is expecting to get his own drinks but a manager is walking around pouring coffee refills, we will have exceeded their expectations.

- Friendly employees — Our employees will be ringing dinner bells when fresh-baked rolls come out of the oven or our signature steaks are ready. Our managers will make table visits a priority, and who knows? Our guests may even see our staff perform a line dance or two! We will dress casually in tailored jeans and ironed logo T-shirts that our customers may purchase for a nominal price.

- Dinner all day on Sat./Sun. — We will feature our dinner menu all day on Saturday and Sunday. Since both days are busy all day long, we will not shut down at midday.

- Reduced dinner pricing — On Monday-Thursday the dinner price will be slightly lower than on Fri./Sat./Sun. since we will add fried shrimp and ribs to the weekend selection.

Company Ownership

Sagebrush Sam’s – “a steak buffet” is a sole proprietor business. Samuel Brooks is the principal owner. It is Mr. Brooks’ intention to offer outside ownership in Sagebrush Sam’s on an equity, debt, or combination basis in order to facilitate the start-up and growth of Sagebrush Sam’s.

Mr. Brooks holds a BS degree in management from the University of Alberta. He has held executive level positions in management with several successful national restaurant chains.

Start-up Summary

Sagebrush Sam’s start-up expenses cover a wide range of items as shown in the following chart and table. Below is the detailed reasoning behind these estimates.

- Kitchen Design — (confidential or proprietary information deleted)…will be doing the kitchen design.

- Architectural Plans — (confidential or proprietary information deleted)…has agreed to do our architectural plans.

- Travel/Lodging — Travel expenses for Sam Brooks to monitor construction, hire, and train staff.

- Manuals/Handbooks/Recipes — All are estimates for typing, printing of employee training information, laminating recipes for kitchen use, and binders for all manuals.

- Pre-opening Labor — This will cover training of employees and management as well as cleaning and organizing the restaurant prior to opening.

- VIP Lunch/Dinner — We will host both a VIP lunch and dinner. This will serve the dual purpose of training our staff and introducing ourselves to the community. The list of individuals invited will come from the Chamber of Commerce. We will pick a local charity to be the beneficiary of our event. A guest will receive an invitation for himself and one other to attend our event free-of-charge. All we will ask of our patrons is that they make a small contribution to the hosting charity. We will run the lunch on Monday, followed by the dinner on Tuesday, with our Grand-Opening on Wednesday.

- Building/Land/Equipment — There are two methods available for the growth of Sagebrush Sam’s. We can build from ground up or we can do conversions from existing or closed restaurants.

| Start-up | |

| Requirements | |

| Start-up Expenses | |

| Kitchen/Architectual Plans | $75,000 |

| Travel and Lodging | $8,000 |

| Design of Logo | $6,500 |

| Manuals/Handbooks/Recipes | $2,420 |

| Recruiter Fees/Help Wanted Ads | $28,500 |

| Pre-opening Labor-staff/Mgmt/Trainers | $72,750 |

| Uniforms | $3,450 |

| VIP Lunch/Dinner | $6,825 |

| Office/Miscellaneous Expenses | $5,500 |

| Total Start-up Expenses | $208,945 |

| Start-up Assets | |

| Cash Required | $160,000 |

| Start-up Inventory | $35,000 |

| Other Current Assets | $100,000 |

| Long-term Assets | $1,500,000 |

| Total Assets | $1,795,000 |

| Total Requirements | $2,003,945 |

| Start-up Funding | |

| Start-up Expenses to Fund | $208,945 |

| Start-up Assets to Fund | $1,795,000 |

| Total Funding Required | $2,003,945 |

| Assets | |

| Non-cash Assets from Start-up | $1,635,000 |

| Cash Requirements from Start-up | $160,000 |

| Additional Cash Raised | $0 |

| Cash Balance on Starting Date | $160,000 |

| Total Assets | $1,795,000 |

| Liabilities and Capital | |

| Liabilities | |

| Current Borrowing | $0 |

| Long-term Liabilities | $0 |

| Accounts Payable (Outstanding Bills) | $0 |

| Other Current Liabilities (interest-free) | $0 |

| Total Liabilities | $0 |

| Capital | |

| Planned Investment | |

| Sam Brooks | $500,000 |

| Investor 2 | $1,503,945 |

| Other | $0 |

| Additional Investment Requirement | $0 |

| Total Planned Investment | $2,003,945 |

| Loss at Start-up (Start-up Expenses) | ($208,945) |

| Total Capital | $1,795,000 |

| Total Capital and Liabilities | $1,795,000 |

| Total Funding | $2,003,945 |

Company Locations and Facilities

Sagebrush Sam’s will range in size from 7,000-10,000 square feet and will seat from 300-400 guests. Each location will feature authentic western antiques such as Native American blankets, cowboy gear, and horse tack. We will equip the restaurant with a state-of-the-art sound system connected to an old-time juke box where our customers will be able to select their favorite country and western songs for free. Every restaurant will be built to our prototype specifications: clean lines, open, and pleasing to the customer.

The site/building selection will be chosen based upon the following list of criteria:

- Community size minimum of 40,000 people within five miles.

- High visibility.

- Easy access to parking lot with a minimum of 120 parking spaces.

- Mid- to low-cost land not to exceed $600,000.

- Heavy blue-collar worker makeup in the community.

- No overabundance of competition in the trade area.

All of these qualities are consistent with Sagebrush Sam’s goal of providing a top quality, entertaining dining experience at an unbelievably low price. We want “word of mouth” to be our best form of marketing, where our guests cannot believe the value of their dining experience and can’t wait to tell their friends and neighbors.

Services

Sagebrush Sam’s will provide quality dining seven days per week. We will only close our locations on Christmas and Thanksgiving. All locations will be open for lunch and dinner. Selected locations will serve breakfast either daily or only on weekends. All meals will be self-serve buffet style offerings for a fixed price.

Competitive Comparison

Sagebrush Sam’s will have broad customer appeal due to our casual family atmosphere, wide variety of food offerings, and low price points. We will not only compete with the casual segment restaurants, but also with the family value steak restaurants.

In competing against the casual theme restaurants, we will have the following advantages:

- Lower price point for a complete meal. If our consumer is a steak lover, his Sagebrush Sam’s meal is almost half what he would pay at a theme restaurant.

- There will be no tipping at Sagebrush Sam’s, since we are self-service. This will reduce the actual customer cost of our dining experience by 10-15%.

- Speed of service will be instant: no waiting for a steak, salad, beverage, or dessert. Everything will be readily available: hot, juicy, fresh, and cooked as requested.

- Our portions will be “just right.” Since we are “all-you-can-eat” the portion size meets the need, rather than a pre-determined amount meant to suit the “average” person.

- Variety is the name of our game. Guests will choose from over 100 different items prepared fresh daily. It is often difficult to meet the dining requests of each family member due to individual tastes. However, at Sagebrush Sam’s, there will be something for everyone, every day of the week.

- We will provide more entertainment than our competition. Our guests will view our meat-cutting cooler as they walk in; they will watch us cooking 70-80 steaks at a time on our mesquite grill; and they will see us preparing and cooking their hot entrees, desserts, and salads. We want our guests to feel a part of the “Sagebrush Sam’s” dining experience!

In competing against the family value steak restaurants, we will have the following advantages:

- We will serve better quality food than our competitors. Nightly, we will offer USDA-choice sirloin steaks that are hand-cut daily and aged for 21 days. With our higher dinner price points, we will feature better quality items on the buffet. Not only can we afford to do this, but it will also limit the amount of steaks that our guests will consume per visit. Even though some guests will eat 4-5 steaks, the average still remains at 1.2 steaks per guest.

- We will offer a lower price point at lunch than our competition and feature a fresh Sam’s Specialty Beefburger, hot and juicy off our display grill, plus the buffet! Our guest could pay the same price at a quick service restaurant, QSR, but only receive a burger, fries, and a drink.

- Our surroundings will be more entertaining than our competitors’.

- Our food will be fresher since we will close weekdays between 2:30 p.m. and 4:00 p.m., and shorter evening hours.

- Our guests will not encounter service problems. Our competitors still feature servers who bring beverages, extra plates, and dinners if ordered. Their servers, which traditionally handle as many as 10 tables at a time, frequently have trouble being everywhere at the same time. With Sagebrush Sam’s, everything is out front and ready for our guests. We will explain our service policy up front and, therefore, never let them down.

- There will be no confusing menu board when guests arrive at our restaurant. One price will be stated, with everything included. Some of our competitors have 10-foot-long menu boards which are overwhelming to customers and difficult to read. Others try to up-sell and ask too many questions while reeling off specials of the day. After all is said and done, they sell 90% buffets and 10% dinners. We’ve made it simple: one price, everything included. And we’ve put steak back on the menu where it belongs — right on top!

- We will not need trays for guests carrying drinks, plates, silverware and napkins from the cash register at Sagebrush Sam’s, everything is conveniently placed in the dining room near the food stations.

- We will be able to staff our restaurant with 25% fewer employees than our competition. With no need for servers, only one cashier, shorter operating hours, and out-front servicing of our food bars, we can efficiently run with a reduced staff.

- There is no tipping at Sagebrush Sam’s, since we are self-service. This will reduce the actual customer cost of our dining experience by 10-15%.

Sales Literature

Currently, there is not any sales literature produced for Sagebrush Sam’s. However there are plans to produce three different pieces once we open. All should be relatively inexpensive to produce and most will be accomplished in-house by using desk top publishing. Below are the pieces that we are planning to produce.

- Table Toppers — will explain concept and differences between lunch/dinner, “Theme Nights,” selling gift certificates, announcing job opportunities, and possibly mentioning franchise possibilities.

- Brochures/Handouts — will explain that we can handle large parties, banquets, or buses; another will list our daily featured entrees.

- Direct Mail Piece — will explain our concept, list prices, and show inside photographs of our restaurant. We will produce and mail this after our first quarter of operation.

Technology

Each Sagebrush Sam’s will invest in a single high-speed computer to provide a fast and efficient connection to the Internet and also be a link to our cash registers. We will then be able to poll each restaurant nightly to our Corporate Support Center and be able to daily digest key financial information. We will also order online, email, and have a Web page.

Future Services

Sagebrush Sam’s plans for slow and cautious growth during its initial start-up phase. We foresee no more than three units within the first three years of operation. Thereafter, we will never develop more units than we have adequate manpower to operate. A second principle in our growth will be to cluster our development. Our first three units will be within a short distance of each other (a three-hour drive). Afterwards, we will work with neighboring geographical areas for development. Thirdly, we will develop one ground-up unit and one conversion with the first three restaurants. This will then allow us to test which model will work best for future, long-term development.

Market Analysis Summary

Sagebrush Sam’s is faced with the exciting opportunity of being the first mover in the “all-you-can-eat steak buffet” concept to become a national player. The consistent popularity of steak, combined with a value price point in a buffet concept, has proven to be a winning concept in other markets and will produce the same results nationally.

In looking at our market analysis, we have defined the following groups as targeted segments. The only exception comes when we define our targeted segment for lunch. We firmly believe, and have witnessed, that a much broader appeal exists for this midday time slot because we have priced it so low and feature our Sam’s Specialty Beefburger. Below are our targeted market segments.

- Age — Seniors, Baby-Boomers, young married couples with children, and blue-collar workers of all ages.

- Family Unit — We will appeal to young families with new babies or mature families with children under the driving age. Most of our family units will have two wage earners.

- Gender — We will equally target both sexes with a slight skew for males due to their heavy consumption of red meat.

- Income — We will appeal to the high side of low income individuals and to all in the middle income bracket.

- Occupation — We will target the blue-collar worker, young professionals with a family, and most of mid-America.

- Education — High school graduates, or individuals with some college.

By our definition, we will have very broad appeal for our concept. It is our goal to be the restaurant of choice for the largest dining audience in America.

Target Market Segment Strategy

Sagebrush Sam’s intends to cater to the bulk of mid-America. We have chosen this group for several important reasons. First and foremost is the sheer size. With our restaurants seating almost 400 people, we will need a broad base and mass appeal to fill them. It is our goal to have “something for everyone” every day on our menu.

Secondly, it is a very heavy restaurant user group. Last year, Americans dined out an average of 3.7 times per week (that’s once every other night). They are on limited or fixed incomes and seek a value/price relationship that will not stretch their budgets.

Lastly, this group will see a large growth in their numbers over the next decade. If we can continue to meet and exceed their expectations, we should witness same store sales growth over this time period. We will, however have to stay focused on their changing needs and menu choices to maintain their loyalty. For the most part, this group is in a hurry, due to heavy time demands at work and home, so our buffet style of service suits them to a “T.”

Our lunch strategy is dual purposed. First, we are featuring fresh ground Sam’s Specialty Beefburgers with all the fixin’s to fill America’s craving for hamburgers. Most folks’ idea of lunch is a quick sandwich, not a heavy meal. Half of our hot food selection will be replaced with sliced tomatoes and onions, pickles and relish, and chopped or leaf lettuce. Our guests will pick up their Sam’s Specialty Beefburger at our display grill, add melted cheese or hot BBQ sauce, and help themselves to the hottest french fries in town seasoned with our special blend of spices. What’s not to like about a hot, juicy Sam’s Specialty Beefburger served right off the grill!!!

Second, we want to keep the price point at lunch as low as possible to keep us in competition with fast-food restaurants. At $…(confidential or proprietary information deleted)…we are only slightly above the QSR segment and we offer much, much more. Not only do our guests get a sandwich, drink, and fries but also a salad, dessert and a selection of hot food items. By reducing the hot food assortment from dinner, we will be able to keep our food cost in line with the reduced price. All in all, this is a win-win strategy that will broaden our customer base at lunch to include singles, teens, and professionals while still maintaining our core market segment.

| Market Analysis | |||||||

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | |||

| Potential Customers | Growth | CAGR | |||||

| Lunch | 6% | 2,888 | 3,061 | 3,245 | 3,440 | 3,646 | 6.00% |

| Senior Dinner | 6% | 932 | 988 | 1,047 | 1,110 | 1,177 | 6.01% |

| Children (3-10) | 6% | 1,406 | 1,490 | 1,579 | 1,674 | 1,774 | 5.98% |

| Weekday Dinner | 6% | 2,172 | 2,302 | 2,440 | 2,586 | 2,741 | 5.99% |

| Weekend Dinner | 6% | 2,958 | 3,135 | 3,323 | 3,522 | 3,733 | 5.99% |

| Total | 5.99% | 10,356 | 10,976 | 11,634 | 12,332 | 13,071 | 5.99% |

Market Needs

Sagebrush Sam’s sees our targeted market group as having many dining dollar needs. Taken from a recent Consumer Reports on Eating Share Trends (CREST) survey, below are the needs we will focus on in Sagebrush Sam’s. Our core group:

- Seeks strong value.

- Wants variety and flavor in its food.

- Looks for speed of service.

- Wants an entertaining dining experience.

- Insists upon a clean, friendly, and attractive dining environment.

Market Survey

A market survey was conducted in February, 2000 (seven months after the opening of the second …(confidential or proprietary information deleted)…steak buffet restaurant by Sam Brooks. Key questions were asked of 505 customers called at random in the surrounding area to determine how they rated their dining experience at the steak buffet concept. Some key findings include: (confidential or proprietary information deleted).

Service Business Analysis

The restaurant industry in the U.S. has experienced rapid growth in the last 20 years and is now moving into the mature stage of its life cycle. Many factors contributed to the large demand for good restaurants in the U.S. today. People want more leisure time. There are more two-wage earner families today, and more discretionary income. The competition is strong, with many formidable chains competing for the consumer dollar. It is almost impossible today to strike off into a new, unique, untried venue. Only the strong will survive and prosper.

Due to intense competition, restauranteurs must look for ways to differentiate their place of business in order to achieve and maintain a competitive advantage. The founder of Sagebrush Sam’s realizes the need for differentiation and strongly believes that combining the popularity of steak with the buffet concept is the key to success. The fact that no other national chain has entered this arena as yet presents us with a window of opportunity and an entrance into a profitable niche in the market.

Competition and Buying Patterns

1999 was a prosperous year for the restaurant industry. While not every chain was as successful as it could be, consumers stepped up and continued to increase their use of restaurants. They appeared to have happily paid a bit more for a meal. They don’t seem to need promotions to be inspired to buy. At the same time, operators, particularly chains, appeared fairly cautious. No incremental units were built for the first time since the early 1990’s. Though there were some rocky points in the American economy over the course of the year, things finished up on a high note, and prospects bode well for 2000.

Gross Domestic Product (GDP) percolated along at a growth rate of roughly 4%. The remarkable thing about the GDP is how strongly it finished the year. Disposable personal income grew a little under the pace it set the past two years. The unemployment rate continued to decline throughout the year, and the Consumer Price Index (CPI) popped above 2% but stayed remarkably low.

Concerns about the sustainability of the current economic boom appear to have had a strong impact on the restaurant industry within the operator community. In 1998, after three years of strong increases, the rate of growth for restaurant units dropped to zero! This is the first time since the recession at the start of the 1990’s that the number of restaurants did not grow.

Among chains as a whole, however, smaller chains (under 99 units) were the ones that saw unit counts decline. The most aggressive growth group remains the chains that number between 100 and 500 units.

The conservative behavior of the operator community might have led to a lackluster year for the industry if it weren’t for the fact that consumers kept right on buying more restaurant prepared foods. In 1999, the number of meals and snacks purchased from a restaurant per person grew to 158 occasions per year (nearly half the days in a year), another all-time high!

The combined boosts in traffic counts and guest check averages resulted in a 6.5% increase in consumer spending at restaurants. The industry has achieved the longest and strongest expenditures growth ever recorded in the 25-year history of CREST.

All in all, 1999 has been a great year for the restaurant industry. Sales are increasing, consumers continue to use restaurants more often and in more situations, and the restaurant companies have managed themselves so that, on balance, they are in a fairly healthy condition. Every segment and every category grew.

Industry Marketing Overview: 1999

In 1999, campaigns focused on the classic themes of value and quality. As a result of the thriving economy, however, chains added additional elements to their campaigns. For instance, chains approached advertising with greater creativity to differentiate themselves within the marketplace. Chains also focused more on customer service.

(Confidential or proprietary information deleted.)

Regardless of the message, consumers perceived operators to be dealing less this year. For the third year in a row, the rate of dealing did not increase. The trend that had never been seen before continues to stretch! This is not all a case of operators offering fewer deals, however. Many of the deals that are offered have been in place for many years. Consumers may no longer perceive combination meals and $0.99 premium sandwiches as deals. The upside of this is that consumers may be sensitive to special deals when they are introduced. The downside is that it’s tough to come up with a price with more magic appeal than $0.99.

Restaurant Industry Long-Term Future

In the near term, it looks as though two things are likely to happen: restaurants may not have the resources to expand as fast as they did in the early 1990’s, and consumers are likely to continue to increase their demand for prepared meals and snacks. Well-thought-out and well-managed restaurant companies have not enjoyed the market valuations that the dot-coms have in the past year. It seems that nothing the industry can do will attract capital the way it did earlier in the 1990’s. In spite of continued same store sales increases, the lack of interest that the industry generates in the financial markets could keep restaurant operators in a conservative frame of mind in the near term. That lack of financial resources combined with the restrictions faced in the labor market should hold unit development back.

These operators will be wondering how to get more out of the real estate they already have. One of the ways to do this is to raise prices. They have been doing this with fair success for the past couple of years and are likely to continue to push the envelope in this respect. In addition, they are likely to want to get into new business segments: expand into breakfast, offer takeout or delivery service, experiment with snacks. Those ideas will require partnership with manufacturers to develop and design those new concepts within the existing chains.

Fortunately, consumers are likely to continue to do their part in the market. Over the long term, consumers have spent about 5% of their disposable personal income on food away from home. That number has stayed almost flat since 1930. Given the stability of this number, you can expect that total spending in the industry will grow no more than a shade faster than income. All prospects look good for income growth so we are likely to see continued 3%-5% growth. That should be plenty of room for everyone, provided people/money are available.

Meeting Tomorrow’s Needs

We must first look at how our population is segmented in order to understand tomorrow’s needs. Below is typically how we segment the various generations.

|

Generation |

Birth Years |

Population |

| Baby Boomers |

1946-1964 |

78 Million |

| Gen X/Baby Bust |

1965-1978 |

44 Million |

| Gen Y/Echo Boom |

1979-1994 |

70 Million |

The good news is that Gen Y is almost the same size as the Baby Boomers. With their numbers so large, our industry will have to cater to their tastes more in the future to continue increasing revenue. This generation will have different tastes and interests; therefore, we will also need to market to them differently.

We will see a gradual menu evolution. Mexican, Tex-Mex, and Italian will play an even larger part in the future. Hot and spicy foods will continue to increase their presence. Chinese and Asian recipes will be the growth of the future. Two very important reasons exist for the rise in food temperature and menu expansion: 81% of the teens today like spicy food, and 79% are very likely to try new foods. (Sagebrush Sam’s “Theme Nights” will cater to these trends.)

We will also see that tomorrow’s consumer will not be as fussy about eating healthy. Below is a table depicting recent consumer trends concerning diet and calorie counting:

|

1990 |

1998 |

|

| Always watch calories |

39% |

26% |

| Limited snacking |

41% |

29% |

| Avoid fat |

51% |

41% |

| Avoid fried foods |

60% |

52% |

We will see an increase in the trend of putting family and food together. The future generations will frequent family-style dining more often. Gen Y sees itself as more stressed, having more time demands, and putting more value on fun. They like customer inter-activity, fun environments, and watching their food cooked to order. This generation is both brand aware and brand loyal.

The biggest challenge facing the restaurant industry in the future will be proper staffing. Not only at issue will be how to recruit a work force, but also how to retain it. Good news, however, is on the horizon, with Gen Y easing the labor crunch. The number of 16-24 year olds in the work force:

- 1982: 24.0 Million

- 1994: 21.6 Million

- 2005: 24.0 Million

With the arrival of the new worker will also come more body piercing and facial hair, as well as the demand for more schedule flexibility and free time. The largest growth area of the labor market will come from the Hispanic-Americans. We will continue to see a decline of the white-American laborer in food service, as this table indicates:

|

1994 |

2005 |

|

| White-American |

71.0% |

66.5% |

| African-American |

11.4% |

11.7% |

| Hispanic-American |

13.1% |

15.3% |

| Asian-American |

4.5% |

6.3% |

It will be up to the wise food service operators to find the right buttons to push in order to retain tomorrow’s worker. What has worked in the past will not work tomorrow. What was once an exceptional benefit yesterday is now the norm or minimum standard today.

What will be the right buttons to push?

- Unlimited options.

- Instant gratification.

- Social consciousness.

- Time pressures.

- Global perspective.

- Complex…

- …and Challenging.

- Ready or not, here they come.

Main Competitors

Everyone that sells prepared meals is our competition because we all compete for the same home meal replacement dollar. However, there are two segments of the restaurant industry that are our main competition: the casual dining steakhouse concept and the family value steak restaurant.

Business Participants

In the United States today, there are 3,349 chain restaurants that compete for the U.S. restaurant dollar. This number does not take into account the thousands of sole proprietor restaurants that dot the American landscape. These chain restaurants accounted for $108,238,150,121 dollars of business in 1999. In the segments that competed against us there were:

- 40 chains in the cafeteria segment

- 1,421 chains in the casual dining segment

- 274 chains in the family dining segment

- 1,676 chains in the quick service segment

Among our closest competitors, six are listed in the largest 200 restaurant chains, ranked by sales volume. All have a large national or strong regional presence.

(Confidential or proprietary information deleted.)

Strategy and Implementation Summary

Our strategy is based on serving our niche markets well. The seniors, baby-boomers, families with young children, blue collar workers, middle income individuals, and most of mid-America can all enjoy the dining experience at Sagebrush Sam’s.

What begins as a customized version of a standard product tailored to the needs of a local clientele can become a niche product that will fill similar needs in markets across the U.S.

We are building an infrastructure so that we can replicate the product, the experience, and the environment across broader geographic lines. Concentration will be on maintaining quality and establishing a strong identity in each local market. The identity becomes the source of “critical mass” upon which expansion efforts are based. Not only does it add marketing muscle but it also becomes the framework for further expansion, using both company-owned and possibly franchised-store locations.

Marketing Strategy

A combination of local media and local store marketing programs will be utilized at each location. Local store marketing is most effective, followed by radio, then print. As soon as a concentration of stores is established in a market, then broader media will be explored.

We believe, however, that the best form of advertising is still “word-of-mouth.” By providing an entertaining environment, with unbeatable quality at an unbelievable price in a clean and friendly restaurant, we will be the talk of the town. Therefore, the execution of our concept is the most critical element of our plan.

Promotion Strategy

We will employ three different marketing tactics to increase customer awareness of Sagebrush Sam’s. Our most important tactic will be word of mouth/in-store marketing. This will be by far the cheapest and most effective of our marketing programs. The second marketing tactic will be Local Store Marketing (LSM). These will be low-budget plans that will provide community support and awareness for our facility. We plan on doing approximately two or three LSM programs per marketing quarter. The last marketing tactic will be local media. This will be the most costly and will be used sparingly to supplement where necessary.

Marketing Programs

Word Of Mouth/In-Store Marketing

- Table tents.

- Wall posters.

- V.I.P. party.

- In-store tour given to every new customer.

- Outdoor marquee message changed weekly.

- Grand Opening celebration.

- Yearly birthday parties.

Local Store Marketing

- School programs – perfect attendance, honor roll.

- Local charity carwash site.

- Customer raffle for western apparel or Sagebrush Sam’s artifacts.

- Free Sagebrush Sam’s “T” shirts to guests that line dance with us.

Local Media

- Direct mail piece – containing interior pictures of our restaurant, our prices, “Theme Nights,” and an explanation of our concept.

- Radio campaign – complete with live remotes on our parking lot. We will pick the three top local stations with which to place our short and catchy ads. We will also sponsor radio call-in contests with free meal coupons to Sagebrush Sam’s as the prize. We will trade our complementary dinner coupons for free radio time. We will also make “live on the air” presentations of our food products to the disk jockeys, hoping to get the reactions broadcast to the listening audience.

- Newspaper campaign – placing several large ads throughout the month to explain our concept to the local area.

- Cable TV – will be a possibility if we can secure favorable rates with enough frequency.

Positioning Statement

Our main focus in marketing will be to increase customer awareness in the surrounding community. We will direct all of our tactics and programs toward the goal of explaining who we are and what we are all about. We have no plans to join in the coupon/discounting wars nor the birthday or frequent buyer clubs upon which others have embarked. We will price our products fairly, keep our standards high, and execute the concept so that word-of-mouth will be our main marketing force.

Furthermore, we will do no outside marketing for the first 90 days of business at each new location. The “honeymoon period” of each opening restaurant will bring in all the guests we can handle properly. It would be a mistake to bring in more customers than we can serve at our peak quality level.

Pricing Strategy

All menu items are moderately priced. (Confidential or proprietary information deleted.) While we are not striving to be the lowest priced restaurant around, we are aiming to be the value leader.

Sales Strategy

The sales strategy is to build and open new locations on schedule in order to increase revenue. Each individual location will continue to build its local customer base over the first three years of operation. The goal is $3-$4 million in annual sales per unit. A unit will be considered mature once it has passed the $3.5 million mark in annual sales.

The following sections illustrate the combined sales forecast.

Sales Programs

Each opening of Sagebrush Sam’s will have the same mix of marketing programs as the others. Below are the programs that we will develop to kick open each location.

- Grand Opening — Each new store will have outdoor signs in place as soon as possible. We want the marquee and road sign to announce that something new and exciting is coming to the neighborhood. Once the shell of the building is up, we will begin mounting large banners announcing that we will open soon. At the grand opening, we will attach rows of pennants to our building, outdoor sign, and pole lights to attract attention. All of this is low cost but has proven to be highly successful.

- VIP Parties — We will host both a VIP lunch and dinner. This will serve the dual purpose of training our staff and introducing ourselves to the community. The list of individuals we invite will come from the Chamber of Commerce. We will choose a local charity to be the beneficiary of our event. All guests will receive an invitation for themselves and one other, to attend our event free-of-charge. All we will ask of our patrons is that they make a small contribution to the hosting charity. We will run the lunch on Monday, followed by the dinner on Tuesday, with our Grand-Opening on Wednesday.

- Point of Purchase (P.O.P.) — We will use table toppers to explain the concept and differences between lunch/dinner, “Theme Nights,” sell gift certificates, announce job openings, and possibly mention franchise opportunities. Brochures and handouts will explain that we can handle large parties, banquets, or buses. Another brochure will list our daily featured entrees.

- Direct Mail Piece — A stand-alone piece measuring 6″ by 7.5″ in size, once folded, will be produced in full color on heavy weight paper. Inside will be all the important details of Sagebrush Sam’s. We will explain our menu, prices, hours of operation, “Theme Nights,” method of service, and provide a locator map.

- Radio — We will create one short, humorous, music-based radio commercial, in both a 30- and a 60-second spot. Both commercials will have a 10-second blank bed where we can mention something specific about the restaurant.

- Newspaper — We will create several different size ads, generic in nature, to be used for any store in the chain.

- Local Store Marketing (LSM) — We have three LSM programs in our current arsenal. We envision having over two dozen LSM promotions for use by individual Sagebrush Sam’s. The three that we will use during the initial marketing wave are the customer raffle, charity carwash (free carwash while you dine with us), and our school program (perfect attendance or honor roll students receive a free meal).

Sales Forecast

Opening day for our first store is scheduled for July 1, 2001.

| Sales Forecast | |||

| Year 1 | Year 2 | Year 3 | |

| Sales | |||

| Lunch | $458,845 | $1,295,843 | $2,511,000 |

| Senior Dinners | $149,659 | $422,659 | $819,000 |

| Child (3-10) | $222,023 | $627,021 | $1,215,000 |

| Weekday Dinner | $312,474 | $882,474 | $1,710,000 |

| Weekend Dinner | $501,605 | $1,416,603 | $2,745,000 |

| Total Sales | $1,644,606 | $4,644,600 | $9,000,000 |

| Direct Cost of Sales | Year 1 | Year 2 | Year 3 |

| Lunch | $160,595 | $453,545 | $878,850 |

| Senior Dinners | $52,380 | $149,930 | $286,650 |

| Child (3-10) | $77,708 | $219,457 | $425,250 |

| Weekday Dinner | $109,366 | $308,866 | $598,500 |

| Weekend Dinner | $175,562 | $495,812 | $960,750 |

| Subtotal Direct Cost of Sales | $575,611 | $1,627,610 | $3,150,000 |

Milestones

The following table lists important milestones, with projected dates, management and budget responsibility. The milestones schedule indicates our emphasis on planning for sales strategies.

| Milestones | |||||

| Milestone | Start Date | End Date | Budget | Manager | Department |

| Grand Opening Materials | 5/1/2001 | 7/1/2001 | $500 | SB | Executive |

| VIP Lunch & Dinner Party | 6/1/2001 | 7/3/2001 | $6,825 | SB | Executive |

| In Store POP – Table Tents, Posters | 4/1/2001 | 7/1/2001 | $2,500 | SB | Executive |

| Direct Mail Piece | 12/1/2001 | 1/1/2002 | $7,500 | SB | Executive |

| Radio | 11/1/2001 | 12/1/2001 | $7,500 | SB | Executive |

| Newspaper | 10/1/2001 | 11/1/2001 | $7,500 | SB | Executive |

| LSM project #1 | 9/1/2001 | 10/1/2001 | $500 | SB | Executive |

| LSM project #2 | 10/1/2001 | 11/1/2001 | $500 | ? | Store Mgmt |

| LSM project #3 | 11/1/2001 | 12/1/2001 | $500 | ? | Store Mgmt |

| LSM project #4 | 12/1/2001 | 1/1/2002 | $500 | ? | Store Mgmt |

| Totals | $34,325 | ||||

Management Summary

The initial management team depends on the founders themselves, with little back-up. As we grow, we will take on additional help in certain key areas. Part of our basic philosophy will be to run our executive management “lean and mean.” We will not add additional overhead until absolutely necessary. This will mean that the initial staff support team will have to “wear many hats,” so to speak. By doing this, we will keep our overhead as low as possible, allowing us to adequately staff our restaurants. This will also allow our business partners to recoup their initial investments as quickly as possible and enjoy a higher return.

At present time, Samuel Brooks is the sole individual firmly committed to the Sagebrush Sam’s concept. Others, who have helped on the development of this business plan, have expressed a desire to join in this venture at the appropriate time.

Other key personnel are the managing partners and management teams at each location. Several candidates have already been identified for the first Sagebrush Sam’s, depending upon location.

No shortage of qualified staff or management from local labor pools in each market area is expected. One of our key principles in site selection is the availability of staff in the immediate area.

Organizational Structure

Future organizational structure will include a director of store operations when store locations exceed five units. We hope that this individual will come out of the ranks of our stores’ proprietor/managing partners. This will provide a supervisory level between the executive level and the store management level.

Currently, we plan to have our accounting and payroll functions done by a contracted bookkeeping service. However, we will constantly monitor this expense and at such time that it is economically feasible, bring this function in-house. Other possible positions that might be added at a later date include marketing director, purchasing agent, controller, director of human resources, director of training/new store opening team coordinator, director of research & development (for new recipes), and administrative assistants.

Operations of individual stores will be the responsibility of the proprietor/managing partner.

Management Team Gaps

Specific opportunities exist in the store operations supervisory area (not needed initially). These people will be recruited when needed in the local market. However, the first key employee needed will be the proprietor/managing partner. This individual will assist in the detail development of the Sagebrush Sam’s concept plus operate the first restaurant. Hiring of this individual is slated during the initial construction phase.

Temporary help has been secured that will assist in the administrative assistant area. This individual will work on the development of all training materials and manuals plus do our correspondence.

Management Team

Sagebrush Sam’s is currently the creative idea solely of Samuel Brooks. As the company is small in nature, it requires a simple organizational structure. Implementation of this organization form calls for Sam Brooks to make all of the major management decisions in addition to monitoring all other business activities.

(Confidential or proprietary information deleted.)

Personnel Plan

The table below shows our initial management staffing estimates.

| Personnel Plan | |||

| Year 1 | Year 2 | Year 3 | |

| Production Personnel | |||

| Proprietor/Managing Partner | $56,252 | $75,000 | $150,000 |

| General Manager | $36,662 | $60,000 | $120,000 |

| Back of House Manager | $24,999 | $45,000 | $90,000 |

| Front of House Manager | $18,330 | $37,500 | $75,000 |

| Assistant Manager | $14,581 | $37,500 | $75,000 |

| Employees | $317,582 | $789,582 | $1,530,000 |

| Subtotal | $468,406 | $1,044,582 | $2,040,000 |

| Sales and Marketing Personnel | |||

| Name or title | $0 | $0 | $0 |

| Other | $0 | $0 | $0 |

| Subtotal | $0 | $0 | $0 |

| General and Administrative Personnel | |||

| President & C.E.O. | $150,000 | $175,000 | $185,000 |

| Administrative Assistant | $2,675 | $18,000 | $19,000 |

| Director of Training | $0 | $0 | $60,000 |

| Controller | $0 | $0 | $40,000 |

| Subtotal | $152,675 | $193,000 | $304,000 |

| Other Personnel | |||

| Name or title | $0 | $0 | $0 |

| Other | $0 | $0 | $0 |

| Subtotal | $0 | $0 | $0 |

| Total People | 36 | 50 | 91 |

| Total Payroll | $621,081 | $1,237,582 | $2,344,000 |

Financial Plan

Sales — Sagebrush Sam’s is basing its projected sales on the assumption that the first unit will open on July 1, 2001. The second restaurant will open on July 1, 2002, followed by the last one opening on January 1, 2003. We have projected sales on the low side using $3 million dollars per year per restaurant. We did not factor in any sales growth for subsequent years.

Cost of Goods Sold — The cost of goods sold was determined by taking actual Profit and Loss statements from various restaurant concepts and then using our pricing structure and guest counts to arrive at costs.

Management Payroll — Figures are based upon the use of five managers per unit at our maximum bonus and salary levels. If we use four managers per restaurant, this will lower our payroll.

Fixed and Variable Expenses — The various fixed and variable expenses were determined by taking actual numbers from several different restaurant concepts.

Marketing Fees — These funds will be used for the production of various marketing materials.

Advertising — These funds will be used, if necessary, to maintain our sales at projected levels. If we are running significantly ahead of our sales projections, then these funds may not be necessary.

Management Fees — We will use these dollars for accounting and payroll services of our firm. As we grow in size, this cost burden will shrink per store due to efficiencies in volume.

Important Assumptions

The financial plan depends on important assumptions, most of which are shown in the following table as annual assumptions. The monthly assumptions are included in the appendix. Interest rates, tax rates, and personnel burden are based on conservative assumptions. Some of the more important underlying assumptions are:

- We assume a strong economy, without a major recession.

- We assume, of course, that there are no unforeseen changes in consumers’ tastes or interests to make our concept less competitive.

| General Assumptions | |||

| Year 1 | Year 2 | Year 3 | |

| Plan Month | 1 | 2 | 3 |

| Current Interest Rate | 10.00% | 10.00% | 10.00% |

| Long-term Interest Rate | 10.00% | 10.00% | 10.00% |

| Tax Rate | 25.42% | 25.00% | 25.42% |

| Other | 0 | 0 | 0 |

Key Financial Indicators

Food costs must be kept at, or below, 35%.

Unit level employee costs must be kept at, or below, 17%.

One of the other important indicators is inventory turnover. In the restaurant business, turnover exceeds 50 per year, with product being purchased and sold often within the week. The only exception to this will be our sirloin steaks, which will be aged at the unit for 21 days.

Above all, controls must be instituted and maintained over multiple store locations.

Sagebrush Sam’s will use state-of-the-art restaurant control and inventory systems. All systems will be computer-based, allowing for accurate off-premises control.

Break-even Analysis

VARIABLE COSTS

- 35.00% – Cost of goods sold.

- 17.00% – Employee payroll.

- 00.25% – Credit card charges.

- 00.33% – Marketing fees.

- 2.00% – Management fees.

- 2.00% – Advertising.

- 2.00% – Management bonus.

- 3.03% – Employee payroll taxes and benefits.

- 1.50% – Paper and cleaning.

- 63.11% – Total variable costs.

ANNUAL FIXED COSTS

- $170,000 – Management salaries.

- $37,000 – Management payroll taxes and benefits.

- $16,410 – Group insurance.

- $137,100 – Controllable expenses minus credit card charges and paper/cleaning.

- $40,208 – Other expenses minus marketing fees, advertising, and management fees.

- $85,000 – Depreciation.

- $485,718 – Total fixed costs.

| Break-even Analysis | |

| Monthly Revenue Break-even | $67,519 |

| Assumptions: | |

| Average Percent Variable Cost | 35% |

| Estimated Monthly Fixed Cost | $43,888 |

Projected Profit and Loss

Projected Profit and Loss Income Statement for the entire company for three years. Estimates for each month of the first year are in the appendix tables.

| Pro Forma Profit and Loss | |||

| Year 1 | Year 2 | Year 3 | |

| Sales | $1,644,606 | $4,644,600 | $9,000,000 |

| Direct Cost of Sales | $575,611 | $1,627,610 | $3,150,000 |

| Production Payroll | $468,406 | $1,044,582 | $2,040,000 |

| Other | $0 | $0 | $0 |

| Total Cost of Sales | $1,044,017 | $2,672,192 | $5,190,000 |

| Gross Margin | $600,589 | $1,972,408 | $3,810,000 |

| Gross Margin % | 36.52% | 42.47% | 42.33% |

| Operating Expenses | |||

| Sales and Marketing Expenses | |||

| Sales and Marketing Payroll | $0 | $0 | $0 |

| Advertising/Promotion | $32,892 | $92,892 | $180,000 |

| Production Expense | $5,427 | $15,327 | $29,700 |

| Miscellaneous | $0 | $0 | $0 |

| Total Sales and Marketing Expenses | $38,319 | $108,219 | $209,700 |

| Sales and Marketing % | 2.33% | 2.33% | 2.33% |

| General and Administrative Expenses | |||

| General and Administrative Payroll | $152,675 | $193,000 | $304,000 |

| Sales and Marketing and Other Expenses | $0 | $0 | $0 |

| Depreciation | $42,504 | $127,500 | $255,000 |

| Fixed Costs | $44,652 | $133,962 | $267,924 |

| Variable Costs | $94,565 | $267,065 | $517,500 |

| Utilities | $40,002 | $120,000 | $240,000 |

| Insurance | $4,002 | $12,000 | $24,000 |

| Rent | $0 | $0 | $0 |

| Payroll Taxes | $109,931 | $219,052 | $414,888 |

| Other General and Administrative Expenses | $0 | $0 | $0 |

| Total General and Administrative Expenses | $488,331 | $1,072,579 | $2,023,312 |

| General and Administrative % | 29.69% | 23.09% | 22.48% |

| Other Expenses: | |||

| Other Payroll | $0 | $0 | $0 |

| Consultants | $0 | $0 | $0 |

| Contract/Consultants | $0 | $0 | $0 |

| Total Other Expenses | $0 | $0 | $0 |

| Other % | 0.00% | 0.00% | 0.00% |

| Total Operating Expenses | $526,651 | $1,180,798 | $2,233,012 |

| Profit Before Interest and Taxes | $73,938 | $791,610 | $1,576,988 |

| EBITDA | $116,442 | $919,110 | $1,831,988 |

| Interest Expense | $0 | $0 | $0 |

| Taxes Incurred | $17,727 | $197,903 | $400,818 |

| Net Profit | $56,212 | $593,708 | $1,176,170 |

| Net Profit/Sales | 3.42% | 12.78% | 13.07% |

Projected Cash Flow

The chart and table below show our cash flow projections. Monthly figures are in the appendix tables.

| Pro Forma Cash Flow | |||

| Year 1 | Year 2 | Year 3 | |

| Cash Received | |||

| Cash from Operations | |||

| Cash Sales | $1,644,606 | $4,644,600 | $9,000,000 |

| Subtotal Cash from Operations | $1,644,606 | $4,644,600 | $9,000,000 |

| Additional Cash Received | |||

| Sales Tax, VAT, HST/GST Received | $0 | $0 | $0 |

| New Current Borrowing | $0 | $0 | $0 |

| New Other Liabilities (interest-free) | $0 | $0 | $0 |

| New Long-term Liabilities | $0 | $0 | $0 |

| Sales of Other Current Assets | $0 | $0 | $0 |

| Sales of Long-term Assets | $0 | $0 | $0 |

| New Investment Received | $0 | $0 | $0 |

| Subtotal Cash Received | $1,644,606 | $4,644,600 | $9,000,000 |

| Expenditures | Year 1 | Year 2 | Year 3 |

| Expenditures from Operations | |||

| Cash Spending | $621,081 | $1,237,582 | $2,344,000 |

| Bill Payments | $817,393 | $3,061,401 | $5,221,404 |

| Subtotal Spent on Operations | $1,438,474 | $4,298,983 | $7,565,404 |

| Additional Cash Spent | |||

| Sales Tax, VAT, HST/GST Paid Out | $0 | $0 | $0 |

| Principal Repayment of Current Borrowing | $0 | $0 | $0 |

| Other Liabilities Principal Repayment | $0 | $0 | $0 |

| Long-term Liabilities Principal Repayment | $0 | $0 | $0 |

| Purchase Other Current Assets | $0 | $0 | $0 |

| Purchase Long-term Assets | $0 | $0 | $0 |

| Dividends | $0 | $0 | $0 |

| Subtotal Cash Spent | $1,438,474 | $4,298,983 | $7,565,404 |

| Net Cash Flow | $206,132 | $345,617 | $1,434,596 |

| Cash Balance | $366,132 | $711,749 | $2,146,344 |

Projected Balance Sheet

The accompanying table presents our year end balance sheet estimates from our first three years. Year one monthly information is included in the appendix tables.

| Pro Forma Balance Sheet | |||

| Year 1 | Year 2 | Year 3 | |

| Assets | |||

| Current Assets | |||

| Cash | $366,132 | $711,749 | $2,146,344 |

| Inventory | $101,063 | $561,795 | $744,178 |

| Other Current Assets | $100,000 | $100,000 | $100,000 |

| Total Current Assets | $567,195 | $1,373,543 | $2,990,522 |

| Long-term Assets | |||

| Long-term Assets | $1,500,000 | $1,500,000 | $1,500,000 |

| Accumulated Depreciation | $42,504 | $170,004 | $425,004 |

| Total Long-term Assets | $1,457,496 | $1,329,996 | $1,074,996 |

| Total Assets | $2,024,691 | $2,703,539 | $4,065,518 |

| Liabilities and Capital | Year 1 | Year 2 | Year 3 |

| Current Liabilities | |||

| Accounts Payable | $173,479 | $258,620 | $444,428 |

| Current Borrowing | $0 | $0 | $0 |

| Other Current Liabilities | $0 | $0 | $0 |

| Subtotal Current Liabilities | $173,479 | $258,620 | $444,428 |

| Long-term Liabilities | $0 | $0 | $0 |

| Total Liabilities | $173,479 | $258,620 | $444,428 |

| Paid-in Capital | $2,003,945 | $2,003,945 | $2,003,945 |

| Retained Earnings | ($208,945) | ($152,733) | $440,974 |

| Earnings | $56,212 | $593,708 | $1,176,170 |

| Total Capital | $1,851,212 | $2,444,919 | $3,621,090 |

| Total Liabilities and Capital | $2,024,691 | $2,703,539 | $4,065,518 |

| Net Worth | $1,851,212 | $2,444,919 | $3,621,090 |

Business Ratios

These business ratios are future estimates based upon current assumptions. Standard industry comparisons are for SIC code 5812, retail eating places.

| Ratio Analysis | ||||

| Year 1 | Year 2 | Year 3 | Industry Profile | |

| Sales Growth | n.a. | 182.41% | 93.77% | 6.96% |

| Percent of Total Assets | ||||

| Inventory | 4.99% | 20.78% | 18.30% | 3.90% |

| Other Current Assets | 4.94% | 3.70% | 2.46% | 28.39% |

| Total Current Assets | 28.01% | 50.81% | 73.56% | 37.68% |

| Long-term Assets | 71.99% | 49.19% | 26.44% | 62.32% |

| Total Assets | 100.00% | 100.00% | 100.00% | 100.00% |

| Current Liabilities | 8.57% | 9.57% | 10.93% | 19.17% |

| Long-term Liabilities | 0.00% | 0.00% | 0.00% | 29.21% |

| Total Liabilities | 8.57% | 9.57% | 10.93% | 48.38% |

| Net Worth | 91.43% | 90.43% | 89.07% | 51.62% |

| Percent of Sales | ||||

| Sales | 100.00% | 100.00% | 100.00% | 100.00% |

| Gross Margin | 36.52% | 42.47% | 42.33% | 59.31% |

| Selling, General & Administrative Expenses | 33.15% | 29.68% | 29.19% | 39.09% |

| Advertising Expenses | 2.00% | 2.00% | 2.00% | 2.75% |

| Profit Before Interest and Taxes | 4.50% | 17.04% | 17.52% | 1.59% |

| Main Ratios | ||||

| Current | 3.27 | 5.31 | 6.73 | 1.26 |

| Quick | 2.69 | 3.14 | 5.05 | 0.87 |

| Total Debt to Total Assets | 8.57% | 9.57% | 10.93% | 3.27% |

| Pre-tax Return on Net Worth | 3.99% | 32.38% | 43.55% | 54.38% |

| Pre-tax Return on Assets | 3.65% | 29.28% | 38.79% | 7.17% |

| Additional Ratios | Year 1 | Year 2 | Year 3 | |

| Net Profit Margin | 3.42% | 12.78% | 13.07% | n.a |

| Return on Equity | 3.04% | 24.28% | 32.48% | n.a |

| Activity Ratios | ||||

| Inventory Turnover | 8.19 | 4.91 | 4.82 | n.a |

| Accounts Payable Turnover | 5.71 | 12.17 | 12.17 | n.a |

| Payment Days | 32 | 25 | 24 | n.a |

| Total Asset Turnover | 0.81 | 1.72 | 2.21 | n.a |

| Debt Ratios | ||||

| Debt to Net Worth | 0.09 | 0.11 | 0.12 | n.a |

| Current Liab. to Liab. | 1.00 | 1.00 | 1.00 | n.a |

| Liquidity Ratios | ||||

| Net Working Capital | $393,716 | $1,114,923 | $2,546,094 | n.a |

| Interest Coverage | 0.00 | 0.00 | 0.00 | n.a |

| Additional Ratios | ||||

| Assets to Sales | 1.23 | 0.58 | 0.45 | n.a |

| Current Debt/Total Assets | 9% | 10% | 11% | n.a |

| Acid Test | 2.69 | 3.14 | 5.05 | n.a |

| Sales/Net Worth | 0.89 | 1.90 | 2.49 | n.a |

| Dividend Payout | 0.00 | 0.00 | 0.00 | n.a |

Appendix

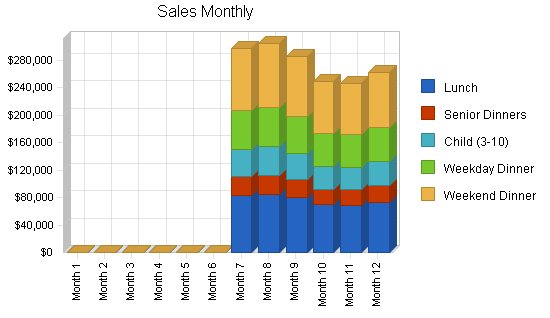

| Sales Forecast | |||||||||||||

| Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | ||

| Sales | |||||||||||||

| Lunch | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $82,947 | $84,956 | $79,682 | $69,304 | $68,718 | $73,238 |

| Senior Dinners | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $27,054 | $27,710 | $25,990 | $22,604 | $22,413 | $23,888 |

| Child (3-10) | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $40,136 | $41,108 | $38,556 | $33,534 | $33,251 | $35,438 |

| Weekday Dinner | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $56,487 | $57,855 | $54,264 | $47,196 | $46,797 | $49,875 |

| Weekend Dinner | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $90,677 | $92,873 | $87,108 | $75,762 | $75,122 | $80,063 |

| Total Sales | $0 | $0 | $0 | $0 | $0 | $0 | $297,301 | $304,502 | $285,600 | $248,400 | $246,301 | $262,502 | |

| Direct Cost of Sales | Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | |

| Lunch | $0 | $0 | $0 | $0 | $0 | $0 | $29,031 | $29,735 | $27,889 | $24,256 | $24,051 | $25,633 | |

| Senior Dinners | $0 | $0 | $0 | $0 | $0 | $0 | $9,469 | $9,698 | $9,096 | $7,911 | $7,845 | $8,361 | |

| Child (3-10) | $0 | $0 | $0 | $0 | $0 | $0 | $14,047 | $14,388 | $13,495 | $11,737 | $11,638 | $12,403 | |

| Weekday Dinner | $0 | $0 | $0 | $0 | $0 | $0 | $19,771 | $20,249 | $18,992 | $16,519 | $16,379 | $17,456 | |

| Weekend Dinner | $0 | $0 | $0 | $0 | $0 | $0 | $31,737 | $32,505 | $30,488 | $26,517 | $26,293 | $28,022 | |

| Subtotal Direct Cost of Sales | $0 | $0 | $0 | $0 | $0 | $0 | $104,055 | $106,575 | $99,960 | $86,940 | $86,206 | $91,875 | |

| Personnel Plan | |||||||||||||

| Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | ||

| Production Personnel | |||||||||||||

| Proprietor/Managing Partner | $0 | $6,250 | $6,250 | $6,250 | $6,250 | $6,250 | $4,167 | $4,167 | $4,167 | $4,167 | $4,167 | $4,167 | |

| General Manager | $0 | $0 | $4,166 | $4,166 | $4,166 | $4,166 | $3,333 | $3,333 | $3,333 | $3,333 | $3,333 | $3,333 | |

| Back of House Manager | $0 | $0 | $0 | $3,333 | $3,333 | $3,333 | $2,500 | $2,500 | $2,500 | $2,500 | $2,500 | $2,500 | |

| Front of House Manager | $0 | $0 | $0 | $0 | $2,916 | $2,916 | $2,083 | $2,083 | $2,083 | $2,083 | $2,083 | $2,083 | |

| Assistant Manager | $0 | $0 | $0 | $0 | $0 | $2,083 | $2,083 | $2,083 | $2,083 | $2,083 | $2,083 | $2,083 | |

| Employees | $0 | $0 | $0 | $0 | $5,000 | $33,000 | $50,541 | $51,765 | $48,552 | $42,228 | $41,871 | $44,625 | |

| Subtotal | $0 | $6,250 | $10,416 | $13,749 | $21,665 | $51,748 | $64,707 | $65,931 | $62,718 | $56,394 | $56,037 | $58,791 | |

| Sales and Marketing Personnel | |||||||||||||

| Name or title | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| General and Administrative Personnel | |||||||||||||

| President & C.E.O. | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | $12,500 | |

| Administrative Assistant | $375 | $165 | $335 | $175 | $50 | $75 | $250 | $250 | $250 | $250 | $250 | $250 | |

| Director of Training | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Controller | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal | $12,875 | $12,665 | $12,835 | $12,675 | $12,550 | $12,575 | $12,750 | $12,750 | $12,750 | $12,750 | $12,750 | $12,750 | |

| Other Personnel | |||||||||||||

| Name or title | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total People | 1 | 3 | 4 | 5 | 6 | 28 | 40 | 41 | 38 | 34 | 34 | 36 | |

| Total Payroll | $12,875 | $18,915 | $23,251 | $26,424 | $34,215 | $64,323 | $77,457 | $78,681 | $75,468 | $69,144 | $68,787 | $71,541 | |

| General Assumptions | |||||||||||||

| Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | ||

| Plan Month | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

| Current Interest Rate | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | |

| Long-term Interest Rate | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | |

| Tax Rate | 30.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | |

| Other | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Pro Forma Profit and Loss | |||||||||||||

| Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | ||

| Sales | $0 | $0 | $0 | $0 | $0 | $0 | $297,301 | $304,502 | $285,600 | $248,400 | $246,301 | $262,502 | |

| Direct Cost of Sales | $0 | $0 | $0 | $0 | $0 | $0 | $104,055 | $106,575 | $99,960 | $86,940 | $86,206 | $91,875 | |

| Production Payroll | $0 | $6,250 | $10,416 | $13,749 | $21,665 | $51,748 | $64,707 | $65,931 | $62,718 | $56,394 | $56,037 | $58,791 | |

| Other | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total Cost of Sales | $0 | $6,250 | $10,416 | $13,749 | $21,665 | $51,748 | $168,762 | $172,506 | $162,678 | $143,334 | $142,243 | $150,666 | |

| Gross Margin | $0 | ($6,250) | ($10,416) | ($13,749) | ($21,665) | ($51,748) | $128,539 | $131,996 | $122,922 | $105,066 | $104,058 | $111,836 | |

| Gross Margin % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 43.24% | 43.35% | 43.04% | 42.30% | 42.25% | 42.60% | |

| Operating Expenses | |||||||||||||

| Sales and Marketing Expenses | |||||||||||||

| Sales and Marketing Payroll | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Advertising/Promotion | 2% | $0 | $0 | $0 | $0 | $0 | $0 | $5,946 | $6,090 | $5,712 | $4,968 | $4,926 | $5,250 |

| Production Expense | 0% | $0 | $0 | $0 | $0 | $0 | $0 | $981 | $1,005 | $942 | $820 | $813 | $866 |

| Miscellaneous | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total Sales and Marketing Expenses | $0 | $0 | $0 | $0 | $0 | $0 | $6,927 | $7,095 | $6,654 | $5,788 | $5,739 | $6,116 | |

| Sales and Marketing % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 2.33% | 2.33% | 2.33% | 2.33% | 2.33% | 2.33% | |

| General and Administrative Expenses | |||||||||||||

| General and Administrative Payroll | $12,875 | $12,665 | $12,835 | $12,675 | $12,550 | $12,575 | $12,750 | $12,750 | $12,750 | $12,750 | $12,750 | $12,750 | |

| Sales and Marketing and Other Expenses | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Depreciation | $0 | $0 | $0 | $0 | $0 | $0 | $7,084 | $7,084 | $7,084 | $7,084 | $7,084 | $7,084 | |

| Fixed Costs | $0 | $0 | $0 | $0 | $0 | $0 | $7,442 | $7,442 | $7,442 | $7,442 | $7,442 | $7,442 | |

| Variable Costs | $0 | $0 | $0 | $0 | $0 | $0 | $17,095 | $17,509 | $16,422 | $14,283 | $14,162 | $15,094 | |

| Utilities | $0 | $0 | $0 | $0 | $0 | $0 | $6,667 | $6,667 | $6,667 | $6,667 | $6,667 | $6,667 | |

| Insurance | $0 | $0 | $0 | $0 | $0 | $0 | $667 | $667 | $667 | $667 | $667 | $667 | |

| Rent | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Payroll Taxes | 18% | $2,279 | $3,348 | $4,115 | $4,677 | $6,056 | $11,385 | $13,710 | $13,927 | $13,358 | $12,238 | $12,175 | $12,663 |

| Other General and Administrative Expenses | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total General and Administrative Expenses | $15,154 | $16,013 | $16,950 | $17,352 | $18,606 | $23,960 | $65,415 | $66,045 | $64,390 | $61,131 | $60,948 | $62,367 | |

| General and Administrative % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 22.00% | 21.69% | 22.55% | 24.61% | 24.75% | 23.76% | |

| Other Expenses: | |||||||||||||

| Other Payroll | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Consultants | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Contract/Consultants | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total Other Expenses | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |

| Total Operating Expenses | $15,154 | $16,013 | $16,950 | $17,352 | $18,606 | $23,960 | $72,342 | $73,140 | $71,044 | $66,919 | $66,686 | $68,483 | |

| Profit Before Interest and Taxes | ($15,154) | ($22,263) | ($27,366) | ($31,101) | ($40,271) | ($75,708) | $56,197 | $58,856 | $51,878 | $38,147 | $37,372 | $43,353 | |

| EBITDA | ($15,154) | ($22,263) | ($27,366) | ($31,101) | ($40,271) | ($75,708) | $63,281 | $65,940 | $58,962 | $45,231 | $44,456 | $50,437 | |

| Interest Expense | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Taxes Incurred | ($4,546) | ($5,566) | ($6,842) | ($7,775) | ($10,068) | ($18,927) | $14,049 | $14,714 | $12,969 | $9,537 | $9,343 | $10,838 | |

| Net Profit | ($10,608) | ($16,697) | ($20,525) | ($23,326) | ($30,203) | ($56,781) | $42,148 | $44,142 | $38,908 | $28,610 | $28,029 | $32,515 | |

| Net Profit/Sales | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 14.18% | 14.50% | 13.62% | 11.52% | 11.38% | 12.39% | |

| Pro Forma Cash Flow | |||||||||||||

| Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | ||

| Cash Received | |||||||||||||

| Cash from Operations | |||||||||||||

| Cash Sales | $0 | $0 | $0 | $0 | $0 | $0 | $297,301 | $304,502 | $285,600 | $248,400 | $246,301 | $262,502 | |

| Subtotal Cash from Operations | $0 | $0 | $0 | $0 | $0 | $0 | $297,301 | $304,502 | $285,600 | $248,400 | $246,301 | $262,502 | |

| Additional Cash Received | |||||||||||||

| Sales Tax, VAT, HST/GST Received | 0.00% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| New Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Other Liabilities (interest-free) | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Long-term Liabilities | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Sales of Other Current Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Sales of Long-term Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Investment Received | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal Cash Received | $0 | $0 | $0 | $0 | $0 | $0 | $297,301 | $304,502 | $285,600 | $248,400 | $246,301 | $262,502 | |

| Expenditures | Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | |

| Expenditures from Operations | |||||||||||||

| Cash Spending | $12,875 | $18,915 | $23,251 | $26,424 | $34,215 | $64,323 | $77,457 | $78,681 | $75,468 | $69,144 | $68,787 | $71,541 | |

| Bill Payments | ($2,267) | ($4,409) | ($4,870) | ($5,734) | ($7,007) | ($11,420) | $1,045 | $247,649 | $176,684 | $155,942 | $129,652 | $142,127 | |

| Subtotal Spent on Operations | $10,608 | $14,506 | $18,381 | $20,690 | $27,208 | $52,903 | $78,502 | $326,330 | $252,152 | $225,086 | $198,439 | $213,668 | |

| Additional Cash Spent | |||||||||||||

| Sales Tax, VAT, HST/GST Paid Out | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Principal Repayment of Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Long-term Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Purchase Other Current Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Purchase Long-term Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Dividends | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal Cash Spent | $10,608 | $14,506 | $18,381 | $20,690 | $27,208 | $52,903 | $78,502 | $326,330 | $252,152 | $225,086 | $198,439 | $213,668 | |

| Net Cash Flow | ($10,608) | ($14,506) | ($18,381) | ($20,690) | ($27,208) | ($52,903) | $218,799 | ($21,828) | $33,448 | $23,314 | $47,862 | $48,834 | |

| Cash Balance | $149,392 | $134,887 | $116,506 | $95,815 | $68,607 | $15,704 | $234,503 | $212,674 | $246,123 | $269,436 | $317,299 | $366,132 | |

| Pro Forma Balance Sheet | |||||||||||||

| Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | ||

| Assets | Starting Balances | ||||||||||||

| Current Assets | |||||||||||||

| Cash | $160,000 | $149,392 | $134,887 | $116,506 | $95,815 | $68,607 | $15,704 | $234,503 | $212,674 | $246,123 | $269,436 | $317,299 | $366,132 |

| Inventory | $35,000 | $35,000 | $35,000 | $35,000 | $35,000 | $35,000 | $35,000 | $114,461 | $117,233 | $109,956 | $95,634 | $94,827 | $101,063 |

| Other Current Assets | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 |

| Total Current Assets | $295,000 | $284,392 | $269,887 | $251,506 | $230,815 | $203,607 | $150,704 | $448,963 | $429,907 | $456,079 | $465,070 | $512,125 | $567,195 |

| Long-term Assets | |||||||||||||

| Long-term Assets | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 |

| Accumulated Depreciation | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $7,084 | $14,168 | $21,252 | $28,336 | $35,420 | $42,504 |

| Total Long-term Assets | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,500,000 | $1,492,916 | $1,485,832 | $1,478,748 | $1,471,664 | $1,464,580 | $1,457,496 |

| Total Assets | $1,795,000 | $1,784,392 | $1,769,887 | $1,751,506 | $1,730,815 | $1,703,607 | $1,650,704 | $1,941,879 | $1,915,739 | $1,934,827 | $1,936,734 | $1,976,705 | $2,024,691 |

| Liabilities and Capital | Month 1 | Month 2 | Month 3 | Month 4 | Month 5 | Month 6 | Month 7 | Month 8 | Month 9 | Month 10 | Month 11 | Month 12 | |

| Current Liabilities | |||||||||||||