Indonesia EEC

Executive Summary

Indonesia EEC is a subsidiary company of United States Energy Engineering & Construction (U.S. EEC) that provides services including engineering, design, procurement, project management, construction and construction management, environmental consulting, management consulting, quality assurance and quality control, information management, operations and maintenance, and process technology development.

U.S. EEC’s management wants Indonesia EEC to deliver a good financial performance. As a subsidiary company of U.S. EEC, Indonesia EEC sets the following objectives for the products and services lines of EPC power generation and power delivery projects:

- Expand customer awareness over the planning period.

- Reduce competition and risks while lowering price levels by establishing a joint venture with a reputable local company who also has experience in performing EPC power projects.

- Pursuing not only EPC prospects, but also BOO, BOT, BLT, B&R, and ECC prospects.

- Utilizing the joint venture company as the main entity of EEC to conduct business in Indonesia, and to provide all aspects of energy engineering services.

2.1 Company Ownership

Indonesia EEC was created as an Indonesian “Perseroan Terbatas” (PT.) corporation based in Jakarta, Indonesia, under the Foreign Investment Laws of Republic of Indonesia. The company is owned entirely by the Energy Engineering & Construction company of U.S (U.S. EEC).

2.2 Company History

EEC has been establishing its presence in the Indonesian market since the 1980s by opening and operating a representative office in Jakarta. It recognized the need for establishing a presence as a local company who meets the specific needs of its prospective customers, as well as its larger, long-term U.S. customers who invested in both Indonesia and the Southeast Asia Region.

Indonesia EEC was founded in 1996. Shares in the company are owned entirely by U.S. EEC.

| Past Performance | |||

| 1996 | 1997 | 1998 | |

| Sales | $50,000,000 | $65,000,000 | $87,500,000 |

| Gross Margin | $23,000,000 | $29,900,000 | $40,250,000 |

| Gross Margin % | 46.00% | 46.00% | 46.00% |

| Operating Expenses | $4,800,000 | $4,850,000 | $4,645,000 |

| Collection Period (days) | 72 | 63 | 63 |

| Balance Sheet | |||

| 1996 | 1997 | 1998 | |

| Current Assets | |||

| Cash | $15,000,000 | $19,500,000 | $26,250,000 |

| Accounts Receivable | $6,112,981 | $7,946,875 | $10,697,716 |

| Other Current Assets | $525,931 | $683,710 | $920,380 |

| Total Current Assets | $21,638,912 | $28,130,585 | $37,868,096 |

| Long-term Assets | |||

| Long-term Assets | $710,837 | $924,089 | $1,243,965 |

| Accumulated Depreciation | $0 | $0 | $0 |

| Total Long-term Assets | $710,837 | $924,089 | $1,243,965 |

| Total Assets | $22,349,749 | $29,054,674 | $39,112,061 |

| Current Liabilities | |||

| Accounts Payable | $2,478,188 | $3,221,644 | $4,336,828 |

| Current Borrowing | $0 | $0 | $0 |

| Other Current Liabilities (interest free) | $0 | $0 | $0 |

| Total Current Liabilities | $2,478,188 | $3,221,644 | $4,336,828 |

| Long-term Liabilities | $0 | $0 | $0 |

| Total Liabilities | $2,478,188 | $3,221,644 | $4,336,828 |

| Paid-in Capital | $1,996,500 | $3,295,460 | $4,743,900 |

| Retained Earnings | $116,967 | $952,048 | $1,781,333 |

| Earnings | $17,758,094 | $21,585,522 | $28,250,000 |

| Total Capital | $19,871,561 | $25,833,030 | $34,775,233 |

| Total Capital and Liabilities | $22,349,749 | $29,054,674 | $39,112,061 |

| Other Inputs | |||

| Payment Days | 30 | 30 | 30 |

| Sales on Credit | $31,098,365 | $40,427,875 | $54,422,140 |

| Receivables Turnover | 5.09 | 5.09 | 5.09 |

2.3 Company Locations and Facilities

The office is located in downton Jakarta, Indonesia. This location provides convenience, being near the airport, but also allows the company room to grow. Currently, Indonesia EEC occupies an 800-square meter space, with offices for each department.

Company Summary

Indonesia EEC is a subsidiary company of United States Energy Engineering & Construction (U.S. EEC) that provides services including engineering, design, procurement, project management, construction and construction management, environmental consulting, management consulting, quality assurance and quality control, information management, operations and maintenance, and process technology development.

U.S. EEC’s management wants Indonesia EEC to deliver a good financial performance. As a subsidiary company of U.S. EEC, Indonesia EEC sets the following objectives for the products and services lines of EPC power generation and power delivery projects:

- Expand customer awareness over the planning period.

- Reduce competition and risks while lowering price levels by establishing a joint venture with a reputable local company who also has experience in performing EPC power projects.

- Pursuing not only EPC prospects, but also BOO, BOT, BLT, B&R, and ECC prospects.

- Utilizing the joint venture company as the main entity of EEC to conduct business in Indonesia, and to provide all aspects of energy engineering services.

2.1 Company Ownership

Indonesia EEC was created as an Indonesian “Perseroan Terbatas” (PT.) corporation based in Jakarta, Indonesia, under the Foreign Investment Laws of Republic of Indonesia. The company is owned entirely by the Energy Engineering & Construction company of U.S (U.S. EEC).

2.2 Company History

EEC has been establishing its presence in the Indonesian market since the 1980s by opening and operating a representative office in Jakarta. It recognized the need for establishing a presence as a local company who meets the specific needs of its prospective customers, as well as its larger, long-term U.S. customers who invested in both Indonesia and the Southeast Asia Region.

Indonesia EEC was founded in 1996. Shares in the company are owned entirely by U.S. EEC.

| Past Performance | |||

| 1996 | 1997 | 1998 | |

| Sales | $50,000,000 | $65,000,000 | $87,500,000 |

| Gross Margin | $23,000,000 | $29,900,000 | $40,250,000 |

| Gross Margin % | 46.00% | 46.00% | 46.00% |

| Operating Expenses | $4,800,000 | $4,850,000 | $4,645,000 |

| Collection Period (days) | 72 | 63 | 63 |

| Balance Sheet | |||

| 1996 | 1997 | 1998 | |

| Current Assets | |||

| Cash | $15,000,000 | $19,500,000 | $26,250,000 |

| Accounts Receivable | $6,112,981 | $7,946,875 | $10,697,716 |

| Other Current Assets | $525,931 | $683,710 | $920,380 |

| Total Current Assets | $21,638,912 | $28,130,585 | $37,868,096 |

| Long-term Assets | |||

| Long-term Assets | $710,837 | $924,089 | $1,243,965 |

| Accumulated Depreciation | $0 | $0 | $0 |

| Total Long-term Assets | $710,837 | $924,089 | $1,243,965 |

| Total Assets | $22,349,749 | $29,054,674 | $39,112,061 |

| Current Liabilities | |||

| Accounts Payable | $2,478,188 | $3,221,644 | $4,336,828 |

| Current Borrowing | $0 | $0 | $0 |

| Other Current Liabilities (interest free) | $0 | $0 | $0 |

| Total Current Liabilities | $2,478,188 | $3,221,644 | $4,336,828 |

| Long-term Liabilities | $0 | $0 | $0 |

| Total Liabilities | $2,478,188 | $3,221,644 | $4,336,828 |

| Paid-in Capital | $1,996,500 | $3,295,460 | $4,743,900 |

| Retained Earnings | $116,967 | $952,048 | $1,781,333 |

| Earnings | $17,758,094 | $21,585,522 | $28,250,000 |

| Total Capital | $19,871,561 | $25,833,030 | $34,775,233 |

| Total Capital and Liabilities | $22,349,749 | $29,054,674 | $39,112,061 |

| Other Inputs | |||

| Payment Days | 30 | 30 | 30 |

| Sales on Credit | $31,098,365 | $40,427,875 | $54,422,140 |

| Receivables Turnover | 5.09 | 5.09 | 5.09 |

2.3 Company Locations and Facilities

The office is located in downton Jakarta, Indonesia. This location provides convenience, being near the airport, but also allows the company room to grow. Currently, Indonesia EEC occupies an 800-square meter space, with offices for each department.

Services

Indonesia EEC offers good quality and cost effective service in engineering, design, procurement, project management, construction and construction management, environmental consulting, management consulting, quality assurance and quality control, information management, operations and maintenance and process technology development.

3.1 Service Description

Indonesia EEC offers expertise in the services it offers. With its variety of services, the company sells them so as to allow clients to choose their preferred benefit(s). These include:

- Engineering & Architect (E&A).

- Engineering & Procurement (E&P).

- Engineering & Construction (E&C).

- Project Management (PM).

3.2 Competitive Comparison

The approach Indonesia EEC will take to differentiate itself is to convert its features into the client’s benefits; the company needs to offer real benefits rather than only define the features to its clients.

The benefits it sells shall include many intangibles: reliability, optimizing the client’s profit potential, confidentiality, guaranteed quality, continuous improvements, technology transfer, and cost effectiveness. Long-term customer satisfaction is the most critical component of the services offered by the company.

It is vital to establish presence in the market and to start making sales on the growing segment. Personal relationships are important and memories are long. It is also vital to keep in mind that it is wrong to wait for recovery before establishing market presence. Project and market development timeframes in Indonesia are lengthy: three to four years or more; however, this timeframe can be compressed by a strong local partner. This implies the need for establishing a joint venture company rather than going it alone. Even under normal circumstances, the company needs to enter the market on the basis of a long-term strategic calculus, with commitment and resources. To every firm which is interested in participating in the Indonesian market, now is the time to enter.

3.3 Sales Literature

The business begins with a general corporate and technical brochure establishing the positioning. This brochure will be provided by U.S. EEC.

3.4 Sourcing

Indonesia EEC works with all the major power plants and power transmission equipment suppliers on a project-by-project basis and will not represent any of them under an exclusive agreement.

It also works with a number of reputable and experienced local engineering and construction companies under either a project-by-project or consortium basis. This is done to reduce competition and risks and to provide clients with competitive pricing without cutting profits, as well as maximizing the local contents, and shifting the responsibility to provide bid bonds, performance bonds, and credit lines to the local partner.

Brought to you by

Create a professional business plan

Using AI and step-by-step instructions

Create Your PlanSecure funding

Validate ideas

Build a strategy

3.5 Technology

As a subsidiary company of U.S. EEC, Indonesia EEC will utilize its parent company’s capabilities, experience, resources, and technologies as follows:

- The world-class leaders in the design and construction of power generation and power transmission facilities.

- Full Engineering, Procurement, and Construction (EPC) capabilities.

- Fossil-fueled power plants EPC, hydropower plants EPC, geothermal power plants EPC, nuclear power plants EPC, and plant services.

- Power plant engineering software and power transmission system engineering software both help ensure lowest cost and design of power generation and transmission facilities.

3.6 Future Services

In the near future, Indonesia EEC will establish a joint venture company with a reputable local company who has experience and capability in performing EPC works of power projects, as well as financial capability, and will broaden the coverage by expanding into additional service areas, e.g., captive power project development and operation.

Market Analysis Summary

In Indonesia, there are twelve market sectors of power generation business in which Indonesia EEC will be seeking prospects on a focused and proactive approach.

The Market Analysis table shows the estimated captive power project values in the dollar per year, within the period of 1999-2003, based on the present circumstances. This table is a live and dynamic table. The numbers of dollars each year could increase as the economy corrects itself.

4.1 Market Segmentation

The potential clients/customers during the five-year implementation of this plan for power generation EPC services are composed of twelve groups:

- Captive power developers (this type of client could be any industrial facilities owner who needs power supply for its own facilities or their subsidiaries in the form of IPP developers)

- Pulp and paper producers

- Textile producers

- Cement mills

- Mining industries

- Shrimp farming

- Sugar producers

- Palm oil producers

- Fertilizer manufacturing

- Petrochemicals

- Oil & Gas Exploration & Production Companies

- Oil Refinery Complexes

It seems reasonable, based on strong fundamentals, that the above twelve sectors have strength to be credible buyers in the Indonesian power business, since their business orientation is focused in the export market leads acceptable development risks.

| Market Analysis | |||||||

| 1999 | 2000 | 2001 | 2002 | 2003 | |||

| Potential Customers | Growth | CAGR | |||||

| Captive Plant Developer | 3% | 54,000,000 | 55,620,000 | 57,288,600 | 59,007,258 | 60,777,476 | 3.00% |

| Pulp & Paper Mills | 15% | 272,000,000 | 312,800,000 | 359,720,000 | 413,678,000 | 475,729,700 | 15.00% |

| Textile Manufacturers | 11% | 218,000,000 | 241,980,000 | 268,597,800 | 298,143,558 | 330,939,349 | 11.00% |

| Cement Mills | 5% | 22,000,000 | 23,100,000 | 24,255,000 | 25,467,750 | 26,741,138 | 5.00% |

| Mining | 18% | 41,000,000 | 48,380,000 | 57,088,400 | 67,364,312 | 79,489,888 | 18.00% |

| Shrimp Farms | 20% | 191,000,000 | 229,200,000 | 275,040,000 | 330,048,000 | 396,057,600 | 20.00% |

| Sugar Mills | 4% | 14,000,000 | 14,560,000 | 15,142,400 | 15,748,096 | 16,378,020 | 4.00% |

| Palm Oil Processing | 5% | 16,000,000 | 16,800,000 | 17,640,000 | 18,522,000 | 19,448,100 | 5.00% |

| Fertilizer Manufacturers | 7% | 136,000,000 | 145,520,000 | 155,706,400 | 166,605,848 | 178,268,257 | 7.00% |

| Petrochemical Processing | 5% | 27,000,000 | 28,350,000 | 29,767,500 | 31,255,875 | 32,818,669 | 5.00% |

| Oil & Gas Fields | 5% | 22,000,000 | 23,100,000 | 24,255,000 | 25,467,750 | 26,741,138 | 5.00% |

| Oil Refineries | 5% | 109,000,000 | 114,450,000 | 120,172,500 | 126,181,125 | 132,490,181 | 5.00% |

| Total | 12.16% | 1,122,000,000 | 1,253,860,000 | 1,404,673,600 | 1,577,489,572 | 1,775,879,516 | 12.16% |

4.2 Target Market Segment Strategy

Indonesia EEC will focus on major electricity consumers in Indonesia who are very demanding regarding reliability of their power supply systems.

The current situation in Indonesia can be characterized by commercial paralysis, policy paralysis, and for the moment, a continuing downward economic drift. But it seems reasonable that the previously listed twelve sectors have strength to be credible buyers in the Indonesian power business, since their business orientation is focused in the export market leads acceptable development risks. The uncertainty lies in how long the country’s economic recovery will take and with what twists and turns in the political and economic structure will offer tremendous opportunities for the the company in developing badly needed, inside-the-fence captive power projects to satisfy the demand. This requirement has not diminished because of the crisis. It even increases due to the government owned power utility (PLN) absence to deliver a reliable and cost effective power system.

For the short term, the company needs to be flexible and creative in pricing and financing its services. Indonesian buyers are likely to be more dependent than ever on supplier financing, and looking for bargains; unfortunately, the current economic erosion situation has put them in a compromising position for bargaining. The company needs to be proactive in assisting its customers in finding sources of financing, inventing creative payment terms or offering a more lenient repayment period, if possible, and looking for ways to cut the price of supplies and services. Barter trade has often been a required element of major government projects, but it would be no surprise to see more emphasis on barter trade in the coming period.

4.3 Service Business Analysis

EPC Contractors in power business range from major global Original Equipment Manufacturers (OEM) of the power generation and transmission plants to the local engineering and construction firms.

4.3.1 Major Local Players

Some major domestic players who are estimated as Indonesia EEC’s potential competitors in the power EPC business are listed below. They are politically well-connected at this time and seem to be aggressively pursuing expansion into other infrastructure markets in Indonesia, most notably in power and industrial plants.

- PT. ABB Energy System Indonesia (PT. ABB-ESI), a joint venture of ABB-CE and PT. PAL, a member of BPIS.

- PT. Rekayasa Industry (PT. RI), a government-owned EPC contractor company under the management of the Directorate of Machineries and Base Metals Industries, Ministry of Industry and Trade. PT. RI is well established in the fertilizer processing field.

- PT. Inti Karya Persada Tehnik (PT. IKPT), a local EPC contractor company. PT. IKPT is well established in the petroleum, petrochemical, and geothermal fields.

- Indonesia Power (previously “PT. PLN (Persero) Pembangkitan Tenaga Listrik Jawa Bali-I), a subsidiary operating company of PT. PLN (Persero) for the western part of the Java-Bali power system.

- PT. PLN (Persero) Pembangkitan Tenaga Listrik Jawa Bali-II (PLN PJB-II), a subsidiary operating company of PT. PLN (Persero) for the eastern part of the Java-Bali power system.

- PT. Tripatra.

- PT. Gunanusa.

- PT. Truba Jurong.

- PT. Pertafenikki.

- PT. Aalborg Sunrod Indonesia.

4.3.2 Major Foreign Players

The following companies are major foreign players in Indonesian power business:

- Original Equipment Manufacturers. They are not fully recognized as competitors; however, these companies are seen to be the strongest competitors in Indonesia: ABB, GE, Westinghouse, Siemens, Rolls-Royce, Ansaldo, Mitsubishi, Fuji, Toshiba, Babcock & Wilcox, GEC Alsthom, Foster Wheeler, Austrian Energy, Cockerill Mechanical Industries (CMI), John Brown Ltd., Kvaerner, Lurgi, Ishikawajima Harima (IHI), Wartsila, Caterpillar, Pielstick, MAN, and Niigata.

- Foreign Engineering/EPC companies: Duke Fluor/Daniels, Stone & Webster, Bechtel, Black & Veatch, Sargent & Lundy, Raytheon (EBASCO), Daelim, Hyundai, SsangYong, Balfour Beatty, Jaako Poyry, BE&K Bechtel, Pekka Hemmi, Simons, JGC Corporation, Kajima Corp., SNC Lavallin, and Chiyoda.

- Trading Companies : Sumitomo Corporation, Marubeni, Mitsubishi Heavy Industries, Kanematsu Corporation, and Mitsui.

4.3.3 Competition and Buying Patterns

Recent analysis indicate that total design cost of power plants in Indonesia has decreased by 12%, while total construction cost of power plants in Indonesia has decreased by 23.59% during this economic turmoil, compared to data recorded in 1996. This analysis is based on the assumptions that the local engineers and laborers salary was increased by 25% at the average exchange rate of US$1 = Rp 7,200. By having a local production capability in Indonesia, Indonesia EEC will be able to take advantage of this situation.

When the joint venture company between Indonesia EEC and its local partner has been established, it will be able to reduce costs and increase profits by having a full-service production office in Indonesia.

The critical issue for establishing a local production capability is the ability of Indonesia EEC to hire, train, and retain highly qualified and motivated Indonesian engineers.

Strategy and Implementation Summary

One of the reasons why captive power has become the most important sector in the Indonesian power market is that the customers need the most reliable and efficient power system to reduce the costs. The PLN subsidized electricity tariff is approximately 40% more expensive, and its disturbance rate is high and getting worse.

Brought to you by

Create a professional business plan

Using AI and step-by-step instructions

Create Your PlanSecure funding

Validate ideas

Build a strategy

Furthermore, PLN’s inability to pay power and natural gas at the prevailing exchange rate has put both PLN and independent power producer (IPP) developers into a very difficult position to move forward with their project implementation between 1999 and 2003. Meanwhile, in line with the government’s export increasing program to strengthen the national reserve funds, many big electricity consumers will face their fast growing demand. This situation will compel many electricity consumers (especially large industrial facilities) to set up their own captive power plants.

As a result of this need, Indonesia EEC will focus its marketing directive on those large, export-oriented, industrial companies.

5.1 Competitive Edge

Indonesia EEC’s overall competitive edge in Indonesia is that it brings its parent company’s name recognition as a “one-stop” services provider encompassing engineering, procurement, construction, and trade financing services. The parent company is seen as having more than one hundred years’ experience in the global industry.

One of the most important key factors in Indonesia EEC’s competitive edge is its expertise in providing access to the trade financing, as follows:

- Obtaining low-cost financing specific to the buyer’s country.

- Obtaining commercial and political risk insurance for non-guaranteed loans.

- Furnishing and processing loan documentation for export credit agencies.

- Preparing grant proposals and feasibility studies required by the funding institution when a company moves into new markets.

- Conducting studies to establish project feasibility.

- Applying for and obtaining final commitment of funds based on feasibility studies.

- Arranging for the best available financing through private national and international banking institutions.

The establishment of a joint venture company between Indonesia EEC and a strong, experienced local engineering and construction company is the most strategic step to overcome the competition by reduced production costs as well as to improve flexibility in penetrating the markets in developing countries, especially the Asia Region.

5.2 Sales Strategy

The captive power market in Indonesia will be focused and integrated with the private customers outside the multilateral/bilateral aid programs. To sell to this type of market, Indonesia EEC needs to have these seven important propositions:

- Proven expertise in project financing arrangements, especially under the barter trade arrangements.

- Direct negotiation approaches with the clients.

- Strategic alliances with a reputable local company who has experience as either an EPC company or developer in Indonesian power sector, capability, and the in-house facilities to perform the detailed engineering, procurement, and construction of power projects.

- Competitiveness in pricing.

- Creative payment terms.

- Contributions in enhancing the local manufacturing sector by making it more efficient and competitive.

- Proven expertise in the EPC of reliable and efficient power system.

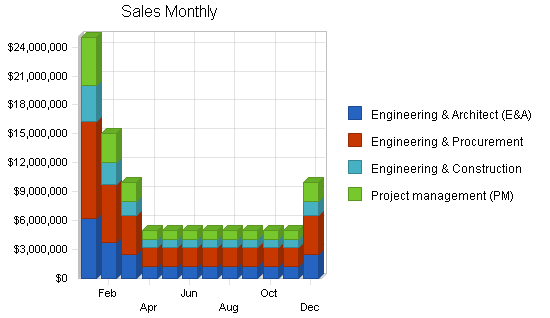

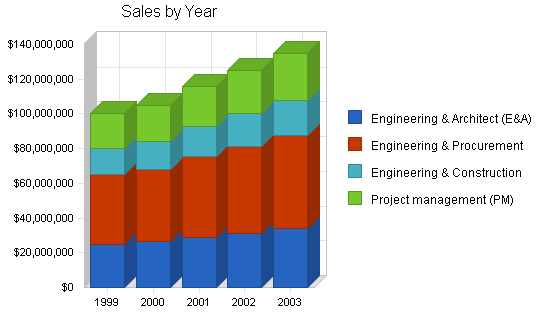

5.2.1 Sales Forecast

We are planning to increase sales substantially in 2001. This is considered reasonable due to the opportunities available in the industry.

January through March 2001 will offer the highest sales, as many clients will begin the implementation of their projects.

| Sales Forecast | |||||

| 1999 | 2000 | 2001 | 2002 | 2003 | |

| Sales | |||||

| Engineering & Architect (E&A) | $25,000,000 | $26,250,000 | $29,000,000 | $31,250,000 | $33,750,000 |

| Engineering & Procurement | $40,000,000 | $42,000,000 | $46,400,000 | $50,000,000 | $54,000,000 |

| Engineering & Construction | $15,000,000 | $15,750,000 | $17,400,000 | $18,750,000 | $20,250,000 |

| Project management (PM) | $20,000,000 | $21,000,000 | $23,200,000 | $25,000,000 | $27,000,000 |

| Total Sales | $100,000,000 | $105,000,000 | $116,000,000 | $125,000,000 | $135,000,000 |

| Direct Cost of Sales | 1999 | 2000 | 2001 | 2002 | 2003 |

| Engineering & Architect (E&A) | $13,500,000 | $14,175,000 | $15,660,000 | $16,875,000 | $18,225,000 |

| Engineering & Procurement | $21,600,000 | $22,680,000 | $25,056,000 | $27,000,000 | $29,160,000 |

| Engineering & Construction | $8,100,000 | $8,505,000 | $9,396,000 | $10,125,000 | $10,935,000 |

| Project management (PM) | $10,800,000 | $11,340,000 | $12,528,000 | $13,500,000 | $14,580,000 |

| Subtotal Direct Cost of Sales | $54,000,000 | $56,700,000 | $62,640,000 | $67,500,000 | $72,900,000 |

Management Summary

Prior to the revenue, Indonesia EEC is led by one president director and two vice presidents (vice president of sales and marketing and vice president of internal business management (IBM)). They will be assisted by one sales manager (who is primarily responsible for sales and market development in power sector), one marketing and business development manager (who is primarily responsible for business development, services development, and research and design), one finance manager, one human resources manager, one accountant, two shared secretaries, one legal officer, one administrative officer, one bookkeeper, and four clerks.

When projects have been secured, then project offices will be established and project personnel and staff will be recruited. Project office organization and staff will encompass the engineering, procurement, and construction divisions.

The administrative section obtains outside services from Indonesian professional firms for tax reporting, legal and contract consulting, and immigration “consultants.” It is expected that these services will continue to be contracted out as the cost of full-time staff positions in these specialists will be large.

6.1 Personnel Plan

Prior to the revenue, the team includes 17 employees, under a president and two vice presidents.

Indonesia EEC’s main management divisions are Sales & Marketing (the marketing, sales, services research and development, and public relations operations will be managed by this division) and Internal Business Management (the legal, accounting, administration, and human resources development sections will be managed by this division).

The following table summarizes our personnel plan for the five years of this business plan.

| Personnel Plan | |||||

| 1999 | 2000 | 2001 | 2002 | 2003 | |

| President Director/Chief Representative | $54,000 | $59,400 | $65,340 | $71,874 | $79,061 |

| Executive Secretary | $6,480 | $7,150 | $7,865 | $8,651 | $9,516 |

| VP Sales & Marketing | $25,992 | $28,600 | $31,460 | $34,606 | $38,066 |

| Sales Manager | $15,600 | $17,160 | $18,876 | $20,764 | $22,840 |

| Marketing & Business Dev. Manager | $15,600 | $17,160 | $18,876 | $20,764 | $22,840 |

| Secretary | $3,900 | $4,290 | $4,719 | $5,191 | $5,710 |

| VP Internal Business Management (IBM) | $25,992 | $28,600 | $31,460 | $34,606 | $38,066 |

| Finance Manager/Senior Accountant | $15,600 | $17,160 | $18,876 | $20,764 | $22,840 |

| Accountant | $12,000 | $13,200 | $14,520 | $15,972 | $17,569 |

| Human Resources Manager | $15,600 | $17,160 | $18,876 | $20,764 | $22,840 |

| Administrative Officer | $12,000 | $13,200 | $14,520 | $15,972 | $17,569 |

| Legal Officer | $12,000 | $13,200 | $14,520 | $15,972 | $17,569 |

| Bookkeeper | $3,900 | $4,290 | $4,719 | $5,191 | $5,710 |

| Clerical | $1,296 | $1,430 | $1,573 | $1,730 | $1,903 |

| Clerical | $1,296 | $1,430 | $1,573 | $1,730 | $1,903 |

| Clerical | $1,296 | $1,430 | $1,573 | $1,730 | $1,903 |

| Clerical | $1,296 | $1,430 | $1,573 | $1,730 | $1,903 |

| Total People | 0 | 0 | 0 | 0 | 0 |

| Total Payroll | $223,848 | $246,290 | $270,919 | $298,011 | $327,808 |

6.2 Legal, Financial and Accounting Status

- Legal Structure: Indonesia EEC is a limited liability Indonesian-registered corporation under Foreign Investment Laws of the Republic of Indonesia.

- Financial and Accounting Status: Operations in Indonesia are not kept in a separate accounting system and the current system does not allow any discrete or accurate information about total costs for local operations.

Financial Plan

The following sections present the financial analysis for Indonesia EEC.

7.1 Important Assumptions

The accompanying table lists Indonesia EEC’s main assumptions for developing its financial projections. The most sensitive assumption is collection days. Indonesia EEC would like to improve collection days to take pressure off of its working capital.

| General Assumptions | |||||

| 1999 | 2000 | 2001 | 2002 | 2003 | |

| Plan Month | 1 | 2 | 3 | 4 | 5 |

| Current Interest Rate | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% |

| Long-term Interest Rate | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% |

| Tax Rate | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% |

| Other | 0 | 0 | 0 | 0 | 0 |

7.2 Break-even Analysis

The following table and chart summarize the Break-even Analysis, including monthly units and sales break-even points.

| Break-even Analysis | |

| Monthly Revenue Break-even | $905,693 |

| Assumptions: | |

| Average Percent Variable Cost | 54% |

| Estimated Monthly Fixed Cost | $416,619 |

7.3 Projected Profit and Loss

The detailed monthly pro-forma income statement for the first year is included in the appendix. The annual estimates are included below.

| Pro Forma Profit and Loss | |||||

| 1999 | 2000 | 2001 | 2002 | 2003 | |

| Sales | $100,000,000 | $105,000,000 | $116,000,000 | $125,000,000 | $135,000,000 |

| Direct Cost of Sales | $54,000,000 | $56,700,000 | $62,640,000 | $67,500,000 | $72,900,000 |

| Power System Studies | $58,000 | $60,900 | $63,945 | $67,142 | $70,499 |

| Total Cost of Sales | $54,058,000 | $56,760,900 | $62,703,945 | $67,567,142 | $72,970,499 |

| Gross Margin | $45,942,000 | $48,239,100 | $53,296,055 | $57,432,858 | $62,029,501 |

| Gross Margin % | 45.94% | 45.94% | 45.94% | 45.95% | 45.95% |

| Expenses | |||||

| Payroll | $223,848 | $246,290 | $270,919 | $298,011 | $327,808 |

| Sales and Marketing and Other Expenses | $4,610,000 | $4,875,000 | $5,430,000 | $5,850,000 | $6,310,000 |

| Depreciation | $0 | $0 | $0 | $0 | $0 |

| Leased Equipment | $6,000 | $6,500 | $7,000 | $7,500 | $8,000 |

| Utilities | $72,000 | $72,000 | $72,000 | $84,000 | $84,000 |

| Insurance | $6,000 | $6,000 | $7,000 | $7,000 | $8,000 |

| Rent | $48,000 | $48,000 | $48,000 | $48,000 | $48,000 |

| Payroll Taxes | $33,577 | $36,944 | $40,638 | $44,702 | $49,171 |

| Other | $0 | $0 | $0 | $0 | $0 |

| Total Operating Expenses | $4,999,425 | $5,290,734 | $5,875,557 | $6,339,213 | $6,834,979 |

| Profit Before Interest and Taxes | $40,942,575 | $42,948,367 | $47,420,498 | $51,093,645 | $55,194,521 |

| EBITDA | $40,942,575 | $42,948,367 | $47,420,498 | $51,093,645 | $55,194,521 |

| Interest Expense | $0 | $0 | $0 | $0 | $0 |

| Taxes Incurred | $10,235,644 | $10,737,092 | $11,855,125 | $12,773,411 | $13,798,630 |

| Net Profit | $30,706,931 | $32,211,275 | $35,565,374 | $38,320,234 | $41,395,891 |

| Net Profit/Sales | 30.71% | 30.68% | 30.66% | 30.66% | 30.66% |

7.4 Projected Cash Flow

Cash flow projections are critical to the company’s success. The monthly cash flow is shown in the chart, with one bar representing the cash flow per month and the other representing the monthly balance. The annual cash flow figures are included here in the following table. Detailed monthly numbers are included in the appendix.

| Pro Forma Cash Flow | |||||

| 1999 | 2000 | 2001 | 2002 | 2003 | |

| Cash Received | |||||

| Cash from Operations | |||||

| Cash Sales | $50,000,000 | $52,500,000 | $58,000,000 | $62,500,000 | $67,500,000 |

| Cash from Receivables | $53,281,049 | $52,129,167 | $57,184,167 | $61,832,500 | $66,758,333 |

| Subtotal Cash from Operations | $103,281,049 | $104,629,167 | $115,184,167 | $124,332,500 | $134,258,333 |

| Additional Cash Received | |||||

| Sales Tax, VAT, HST/GST Received | $0 | $0 | $0 | $0 | $0 |

| New Current Borrowing | $0 | $0 | $0 | $0 | $0 |

| New Other Liabilities (interest-free) | $0 | $0 | $0 | $0 | $0 |

| New Long-term Liabilities | $0 | $0 | $0 | $0 | $0 |

| Sales of Other Current Assets | $0 | $0 | $0 | $0 | $0 |

| Sales of Long-term Assets | $0 | $0 | $0 | $0 | $0 |

| New Investment Received | $0 | $0 | $0 | $0 | $0 |

| Subtotal Cash Received | $103,281,049 | $104,629,167 | $115,184,167 | $124,332,500 | $134,258,333 |

| Expenditures | 1999 | 2000 | 2001 | 2002 | 2003 |

| Expenditures from Operations | |||||

| Cash Spending | $223,848 | $246,290 | $270,919 | $298,011 | $327,808 |

| Bill Payments | $66,791,937 | $73,194,155 | $79,537,301 | $85,870,683 | $92,709,626 |

| Subtotal Spent on Operations | $67,015,785 | $73,440,445 | $79,808,220 | $86,168,694 | $93,037,434 |

| Additional Cash Spent | |||||

| Sales Tax, VAT, HST/GST Paid Out | $0 | $0 | $0 | $0 | $0 |

| Principal Repayment of Current Borrowing | $0 | $0 | $0 | $0 | $0 |

| Other Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 |

| Long-term Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 |

| Purchase Other Current Assets | $0 | $0 | $0 | $0 | $0 |

| Purchase Long-term Assets | $0 | $0 | $0 | $0 | $0 |

| Dividends | $0 | $0 | $0 | $0 | $0 |

| Subtotal Cash Spent | $67,015,785 | $73,440,445 | $79,808,220 | $86,168,694 | $93,037,434 |

| Net Cash Flow | $36,265,265 | $31,188,721 | $35,375,946 | $38,163,806 | $41,220,899 |

| Cash Balance | $62,515,265 | $93,703,986 | $129,079,932 | $167,243,738 | $208,464,638 |

Brought to you by

Create a professional business plan

Using AI and step-by-step instructions

Create Your PlanSecure funding

Validate ideas

Build a strategy

7.5 Projected Balance Sheet

The following Balance Sheet table shows healthy growth of net worth and a strong financial position. The monthly estimates are included in the appendix.

| Pro Forma Balance Sheet | |||||

| 1999 | 2000 | 2001 | 2002 | 2003 | |

| Assets | |||||

| Current Assets | |||||

| Cash | $62,515,265 | $93,703,986 | $129,079,932 | $167,243,738 | $208,464,638 |

| Accounts Receivable | $7,416,667 | $7,787,500 | $8,603,333 | $9,270,833 | $10,012,500 |

| Other Current Assets | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 |

| Total Current Assets | $70,852,311 | $102,411,866 | $138,603,645 | $177,434,952 | $219,397,518 |

| Long-term Assets | |||||

| Long-term Assets | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 |

| Accumulated Depreciation | $0 | $0 | $0 | $0 | $0 |

| Total Long-term Assets | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 |

| Total Assets | $72,096,276 | $103,655,831 | $139,847,610 | $178,678,917 | $220,641,483 |

| Liabilities and Capital | 1999 | 2000 | 2001 | 2002 | 2003 |

| Current Liabilities | |||||

| Accounts Payable | $6,614,112 | $5,962,392 | $6,588,798 | $7,099,870 | $7,666,545 |

| Current Borrowing | $0 | $0 | $0 | $0 | $0 |

| Other Current Liabilities | $0 | $0 | $0 | $0 | $0 |

| Subtotal Current Liabilities | $6,614,112 | $5,962,392 | $6,588,798 | $7,099,870 | $7,666,545 |

| Long-term Liabilities | $0 | $0 | $0 | $0 | $0 |

| Total Liabilities | $6,614,112 | $5,962,392 | $6,588,798 | $7,099,870 | $7,666,545 |

| Paid-in Capital | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 |

| Retained Earnings | $30,031,333 | $60,738,264 | $92,949,539 | $128,514,913 | $166,835,146 |

| Earnings | $30,706,931 | $32,211,275 | $35,565,374 | $38,320,234 | $41,395,891 |

| Total Capital | $65,482,164 | $97,693,439 | $133,258,813 | $171,579,046 | $212,974,937 |

| Total Liabilities and Capital | $72,096,276 | $103,655,831 | $139,847,610 | $178,678,917 | $220,641,483 |

| Net Worth | $65,482,164 | $97,693,439 | $133,258,813 | $171,579,046 | $212,974,937 |

7.6 Business Ratios

Business ratios for the years of this plan are shown below. Industry profile ratios based on the Standard Industrial Classification (SIC) code 8711, Engineering Services, are shown for comparison.

| Ratio Analysis | ||||||

| 1999 | 2000 | 2001 | 2002 | 2003 | Industry Profile | |

| Sales Growth | 14.29% | 5.00% | 10.48% | 7.76% | 8.00% | 7.10% |

| Percent of Total Assets | ||||||

| Accounts Receivable | 10.29% | 7.51% | 6.15% | 5.19% | 4.54% | 35.40% |

| Other Current Assets | 1.28% | 0.89% | 0.66% | 0.52% | 0.42% | 38.30% |

| Total Current Assets | 98.27% | 98.80% | 99.11% | 99.30% | 99.44% | 77.40% |

| Long-term Assets | 1.73% | 1.20% | 0.89% | 0.70% | 0.56% | 22.60% |

| Total Assets | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% |

| Current Liabilities | 9.17% | 5.75% | 4.71% | 3.97% | 3.47% | 44.50% |

| Long-term Liabilities | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 11.70% |

| Total Liabilities | 9.17% | 5.75% | 4.71% | 3.97% | 3.47% | 56.20% |

| Net Worth | 90.83% | 94.25% | 95.29% | 96.03% | 96.53% | 43.80% |

| Percent of Sales | ||||||

| Sales | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% |

| Gross Margin | 45.94% | 45.94% | 45.94% | 45.95% | 45.95% | 0.00% |

| Selling, General & Administrative Expenses | 15.24% | 15.26% | 15.29% | 15.29% | 15.28% | 81.80% |

| Advertising Expenses | 0.03% | 0.04% | 0.04% | 0.04% | 0.04% | 0.20% |

| Profit Before Interest and Taxes | 40.94% | 40.90% | 40.88% | 40.87% | 40.88% | 2.50% |

| Main Ratios | ||||||

| Current | 10.71 | 17.18 | 21.04 | 24.99 | 28.62 | 1.69 |

| Quick | 10.71 | 17.18 | 21.04 | 24.99 | 28.62 | 1.37 |

| Total Debt to Total Assets | 9.17% | 5.75% | 4.71% | 3.97% | 3.47% | 56.20% |

| Pre-tax Return on Net Worth | 62.52% | 43.96% | 35.59% | 29.78% | 25.92% | 6.00% |

| Pre-tax Return on Assets | 56.79% | 41.43% | 33.91% | 28.60% | 25.02% | 13.60% |

| Additional Ratios | 1999 | 2000 | 2001 | 2002 | 2003 | |

| Net Profit Margin | 30.71% | 30.68% | 30.66% | 30.66% | 30.66% | n.a |

| Return on Equity | 46.89% | 32.97% | 26.69% | 22.33% | 19.44% | n.a |

| Activity Ratios | ||||||

| Accounts Receivable Turnover | 6.74 | 6.74 | 6.74 | 6.74 | 6.74 | n.a |

| Collection Days | 60 | 53 | 52 | 52 | 52 | n.a |

| Accounts Payable Turnover | 10.44 | 12.17 | 12.17 | 12.17 | 12.17 | n.a |

| Payment Days | 29 | 32 | 29 | 29 | 29 | n.a |

| Total Asset Turnover | 1.39 | 1.01 | 0.83 | 0.70 | 0.61 | n.a |

| Debt Ratios | ||||||

| Debt to Net Worth | 0.10 | 0.06 | 0.05 | 0.04 | 0.04 | n.a |

| Current Liab. to Liab. | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | n.a |

| Liquidity Ratios | ||||||

| Net Working Capital | $64,238,199 | $96,449,474 | $132,014,848 | $170,335,081 | $211,730,972 | n.a |

| Interest Coverage | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | n.a |

| Additional Ratios | ||||||

| Assets to Sales | 0.72 | 0.99 | 1.21 | 1.43 | 1.63 | n.a |

| Current Debt/Total Assets | 9% | 6% | 5% | 4% | 3% | n.a |

| Acid Test | 9.59 | 15.87 | 19.73 | 23.69 | 27.31 | n.a |

| Sales/Net Worth | 1.53 | 1.07 | 0.87 | 0.73 | 0.63 | n.a |

| Dividend Payout | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | n.a |

Appendix

| Sales Forecast | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Sales | |||||||||||||

| Engineering & Architect (E&A) | 0% | $6,250,000 | $3,750,000 | $2,500,000 | $1,250,000 | $1,250,000 | $1,250,000 | $1,250,000 | $1,250,000 | $1,250,000 | $1,250,000 | $1,250,000 | $2,500,000 |

| Engineering & Procurement | 0% | $10,000,000 | $6,000,000 | $4,000,000 | $2,000,000 | $2,000,000 | $2,000,000 | $2,000,000 | $2,000,000 | $2,000,000 | $2,000,000 | $2,000,000 | $4,000,000 |

| Engineering & Construction | 0% | $3,750,000 | $2,250,000 | $1,500,000 | $750,000 | $750,000 | $750,000 | $750,000 | $750,000 | $750,000 | $750,000 | $750,000 | $1,500,000 |

| Project management (PM) | 0% | $5,000,000 | $3,000,000 | $2,000,000 | $1,000,000 | $1,000,000 | $1,000,000 | $1,000,000 | $1,000,000 | $1,000,000 | $1,000,000 | $1,000,000 | $2,000,000 |

| Total Sales | $25,000,000 | $15,000,000 | $10,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $10,000,000 | |

| Direct Cost of Sales | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |

| Engineering & Architect (E&A) | $3,375,000 | $2,025,000 | $1,350,000 | $675,000 | $675,000 | $675,000 | $675,000 | $675,000 | $675,000 | $675,000 | $675,000 | $1,350,000 | |

| Engineering & Procurement | $5,400,000 | $3,240,000 | $2,160,000 | $1,080,000 | $1,080,000 | $1,080,000 | $1,080,000 | $1,080,000 | $1,080,000 | $1,080,000 | $1,080,000 | $2,160,000 | |

| Engineering & Construction | $2,025,000 | $1,215,000 | $810,000 | $405,000 | $405,000 | $405,000 | $405,000 | $405,000 | $405,000 | $405,000 | $405,000 | $810,000 | |

| Project management (PM) | $2,700,000 | $1,620,000 | $1,080,000 | $540,000 | $540,000 | $540,000 | $540,000 | $540,000 | $540,000 | $540,000 | $540,000 | $1,080,000 | |

| Subtotal Direct Cost of Sales | $13,500,000 | $8,100,000 | $5,400,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $5,400,000 | |

| Personnel Plan | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| President Director/Chief Representative | 0% | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 | $4,500 |

| Executive Secretary | 0% | $540 | $540 | $540 | $540 | $540 | $540 | $540 | $540 | $540 | $540 | $540 | $540 |

| VP Sales & Marketing | 0% | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 |

| Sales Manager | 0% | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 |

| Marketing & Business Dev. Manager | 0% | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 |

| Secretary | 0% | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 |

| VP Internal Business Management (IBM) | 0% | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 | $2,166 |

| Finance Manager/Senior Accountant | 0% | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 |

| Accountant | 0% | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 |

| Human Resources Manager | 0% | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 | $1,300 |

| Administrative Officer | 0% | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 |

| Legal Officer | 0% | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 | $1,000 |

| Bookkeeper | 0% | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 | $325 |

| Clerical | 0% | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 |

| Clerical | 0% | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 |

| Clerical | 0% | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 |

| Clerical | 0% | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 | $108 |

| Total People | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Total Payroll | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | |

| General Assumptions | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Plan Month | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

| Current Interest Rate | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | 8.50% | |

| Long-term Interest Rate | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | 9.00% | |

| Tax Rate | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | |

| Other | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Pro Forma Profit and Loss | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Sales | $25,000,000 | $15,000,000 | $10,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $10,000,000 | |

| Direct Cost of Sales | $13,500,000 | $8,100,000 | $5,400,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $2,700,000 | $5,400,000 | |

| Power System Studies | $5,000 | $5,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $0 | $0 | |

| Total Cost of Sales | $13,505,000 | $8,105,000 | $5,406,000 | $2,706,000 | $2,706,000 | $2,706,000 | $2,706,000 | $2,706,000 | $2,706,000 | $2,706,000 | $2,700,000 | $5,400,000 | |

| Gross Margin | $11,495,000 | $6,895,000 | $4,594,000 | $2,294,000 | $2,294,000 | $2,294,000 | $2,294,000 | $2,294,000 | $2,294,000 | $2,294,000 | $2,300,000 | $4,600,000 | |

| Gross Margin % | 45.98% | 45.97% | 45.94% | 45.88% | 45.88% | 45.88% | 45.88% | 45.88% | 45.88% | 45.88% | 46.00% | 46.00% | |

| Expenses | |||||||||||||

| Payroll | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | |

| Sales and Marketing and Other Expenses | $388,500 | $382,000 | $382,000 | $388,500 | $382,000 | $382,000 | $388,500 | $382,000 | $382,000 | $388,500 | $382,000 | $382,000 | |

| Depreciation | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Leased Equipment | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | |

| Utilities | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | $6,000 | |

| Insurance | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | $500 | |

| Rent | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | $4,000 | |

| Payroll Taxes | 15% | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 | $2,798 |

| Other | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total Operating Expenses | $420,952 | $414,452 | $414,452 | $420,952 | $414,452 | $414,452 | $420,952 | $414,452 | $414,452 | $420,952 | $414,452 | $414,452 | |

| Profit Before Interest and Taxes | $11,074,048 | $6,480,548 | $4,179,548 | $1,873,048 | $1,879,548 | $1,879,548 | $1,873,048 | $1,879,548 | $1,879,548 | $1,873,048 | $1,885,548 | $4,185,548 | |

| EBITDA | $11,074,048 | $6,480,548 | $4,179,548 | $1,873,048 | $1,879,548 | $1,879,548 | $1,873,048 | $1,879,548 | $1,879,548 | $1,873,048 | $1,885,548 | $4,185,548 | |

| Interest Expense | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Taxes Incurred | $2,768,512 | $1,620,137 | $1,044,887 | $468,262 | $469,887 | $469,887 | $468,262 | $469,887 | $469,887 | $468,262 | $471,387 | $1,046,387 | |

| Net Profit | $8,305,536 | $4,860,411 | $3,134,661 | $1,404,786 | $1,409,661 | $1,409,661 | $1,404,786 | $1,409,661 | $1,409,661 | $1,404,786 | $1,414,161 | $3,139,161 | |

| Net Profit/Sales | 33.22% | 32.40% | 31.35% | 28.10% | 28.19% | 28.19% | 28.10% | 28.19% | 28.19% | 28.10% | 28.28% | 31.39% | |

| Pro Forma Cash Flow | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Cash Received | |||||||||||||

| Cash from Operations | |||||||||||||

| Cash Sales | $12,500,000 | $7,500,000 | $5,000,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $5,000,000 | |

| Cash from Receivables | $5,348,858 | $5,765,525 | $12,333,333 | $7,416,667 | $4,916,667 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | $2,500,000 | |

| Subtotal Cash from Operations | $17,848,858 | $13,265,525 | $17,333,333 | $9,916,667 | $7,416,667 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $7,500,000 | |

| Additional Cash Received | |||||||||||||

| Sales Tax, VAT, HST/GST Received | 0.00% | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| New Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Other Liabilities (interest-free) | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Long-term Liabilities | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Sales of Other Current Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Sales of Long-term Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| New Investment Received | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal Cash Received | $17,848,858 | $13,265,525 | $17,333,333 | $9,916,667 | $7,416,667 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $5,000,000 | $7,500,000 | |

| Expenditures | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |

| Expenditures from Operations | |||||||||||||

| Cash Spending | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | $18,654 | |

| Bill Payments | $4,892,688 | $16,457,314 | $10,011,793 | $6,737,681 | $3,576,398 | $3,571,685 | $3,571,848 | $3,576,398 | $3,571,685 | $3,571,848 | $3,576,248 | $3,676,352 | |

| Subtotal Spent on Operations | $4,911,342 | $16,475,968 | $10,030,447 | $6,756,335 | $3,595,052 | $3,590,339 | $3,590,502 | $3,595,052 | $3,590,339 | $3,590,502 | $3,594,902 | $3,695,006 | |

| Additional Cash Spent | |||||||||||||

| Sales Tax, VAT, HST/GST Paid Out | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Principal Repayment of Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Other Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Long-term Liabilities Principal Repayment | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Purchase Other Current Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Purchase Long-term Assets | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Dividends | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | |

| Subtotal Cash Spent | $4,911,342 | $16,475,968 | $10,030,447 | $6,756,335 | $3,595,052 | $3,590,339 | $3,590,502 | $3,595,052 | $3,590,339 | $3,590,502 | $3,594,902 | $3,695,006 | |

| Net Cash Flow | $12,937,516 | ($3,210,444) | $7,302,886 | $3,160,332 | $3,821,615 | $1,409,661 | $1,409,498 | $1,404,948 | $1,409,661 | $1,409,498 | $1,405,098 | $3,804,994 | |

| Cash Balance | $39,187,516 | $35,977,072 | $43,279,958 | $46,440,290 | $50,261,905 | $51,671,566 | $53,081,064 | $54,486,013 | $55,895,674 | $57,305,172 | $58,710,270 | $62,515,265 | |

| Pro Forma Balance Sheet | |||||||||||||

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | ||

| Assets | Starting Balances | ||||||||||||

| Current Assets | |||||||||||||

| Cash | $26,250,000 | $39,187,516 | $35,977,072 | $43,279,958 | $46,440,290 | $50,261,905 | $51,671,566 | $53,081,064 | $54,486,013 | $55,895,674 | $57,305,172 | $58,710,270 | $62,515,265 |

| Accounts Receivable | $10,697,716 | $17,848,858 | $19,583,333 | $12,250,000 | $7,333,333 | $4,916,667 | $4,916,667 | $4,916,667 | $4,916,667 | $4,916,667 | $4,916,667 | $4,916,667 | $7,416,667 |

| Other Current Assets | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 | $920,380 |

| Total Current Assets | $37,868,096 | $57,956,754 | $56,480,785 | $56,450,338 | $54,694,003 | $56,098,952 | $57,508,612 | $58,918,111 | $60,323,059 | $61,732,720 | $63,142,219 | $64,547,317 | $70,852,311 |

| Long-term Assets | |||||||||||||

| Long-term Assets | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 |

| Accumulated Depreciation | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Long-term Assets | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 | $1,243,965 |

| Total Assets | $39,112,061 | $59,200,719 | $57,724,750 | $57,694,303 | $55,937,968 | $57,342,917 | $58,752,577 | $60,162,076 | $61,567,024 | $62,976,685 | $64,386,184 | $65,791,282 | $72,096,276 |

| Liabilities and Capital | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |

| Current Liabilities | |||||||||||||

| Accounts Payable | $4,336,828 | $16,119,950 | $9,783,571 | $6,618,462 | $3,457,341 | $3,452,629 | $3,452,629 | $3,457,341 | $3,452,629 | $3,452,629 | $3,457,341 | $3,448,279 | $6,614,112 |

| Current Borrowing | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Other Current Liabilities | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Subtotal Current Liabilities | $4,336,828 | $16,119,950 | $9,783,571 | $6,618,462 | $3,457,341 | $3,452,629 | $3,452,629 | $3,457,341 | $3,452,629 | $3,452,629 | $3,457,341 | $3,448,279 | $6,614,112 |

| Long-term Liabilities | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Liabilities | $4,336,828 | $16,119,950 | $9,783,571 | $6,618,462 | $3,457,341 | $3,452,629 | $3,452,629 | $3,457,341 | $3,452,629 | $3,452,629 | $3,457,341 | $3,448,279 | $6,614,112 |

| Paid-in Capital | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 | $4,743,900 |

| Retained Earnings | $1,781,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 | $30,031,333 |

| Earnings | $28,250,000 | $8,305,536 | $13,165,947 | $16,300,608 | $17,705,394 | $19,115,055 | $20,524,716 | $21,929,501 | $23,339,162 | $24,748,823 | $26,153,609 | $27,567,770 | $30,706,931 |

| Total Capital | $34,775,233 | $43,080,769 | $47,941,180 | $51,075,841 | $52,480,627 | $53,890,288 | $55,299,949 | $56,704,734 | $58,114,395 | $59,524,056 | $60,928,842 | $62,343,003 | $65,482,164 |

| Total Liabilities and Capital | $39,112,061 | $59,200,719 | $57,724,750 | $57,694,303 | $55,937,968 | $57,342,917 | $58,752,577 | $60,162,076 | $61,567,024 | $62,976,685 | $64,386,184 | $65,791,282 | $72,096,276 |

| Net Worth | $34,775,233 | $43,080,769 | $47,941,180 | $51,075,841 | $52,480,627 | $53,890,288 | $55,299,949 | $56,704,734 | $58,114,395 | $59,524,056 | $60,928,842 | $62,343,003 | $65,482,164 |